Outlook 2024: India’s moment of reckoning?

India has the potential to not only regain its competitive edge but also emerge as a global leader in the textile and apparel sector, affirms Dip Naskar.

The global textile and apparel (T&A) market has went through a roller-coaster ride in the past years, starting from the COVID-19 years to the Russia- Ukraine war, the market has witnessed some level of volatility in recent years. Considering the contraction of the market due to the pandemic in 2020-21, it recovered to a larger extent in 2021 -22. However, there came another setback in the shape of the Russia – Ukraine war and global demand slowdown for the year 2022-23. T&A market is resilient as is expected to take a much better shape in coming years. On the other hand, major buyers are looking to reduce their dependency on China, and thus, looking for China +1 option, combination of the both factors open up an opportunity window for India as well as other nations to capitalise on the emerging market trend. The article will speak about the present situation and more about opportunities in coming year for T&A industry.

Textile & Apparel (T&A) market is growing in long term perspective and evolving

The present global T&A market value is $ 910 billion and recorded a steady CAGR of 3 per cent from 2017 – 2022, a testament to its enduring significance in the global economy. Looking ahead, the industry shows no signs of slowing down, as it is poised to accelerate with a projected CAGR of 4 per cent in the coming years. This promising growth trajectory underscores the industry’s ability to adapt with the evolving global trade dynamics. Apparel trade has undeniably been a dominant force within the global T&A market, commanding a substantial 57 per cent share, which is followed by fabric at 17 per cent for the year 2022. Major apparel exporting countries include China, Bangladesh, Vietnam, Turkey and India.

While the T&A trade is poised for long-term growth, it also faces various challenges. The industry must navigate issues such as supply chain disruptions, changing regulations, and the need to embrace sustainable practices. However, these challenges present opportunities for innovative solutions and forward-thinking businesses. As the global T&A trade continues to expand, it presents not only opportunities but also responsibilities for industry stakeholders to shape a more sustainable and equitable future for fashion and textiles on a global scale.

The below graph indicates the global trade data from the year 2010 till 2022, while it also projects for the year 2025, it also highlights the share of various traded commodities worldwide.

India has indeed been a significant player in the global T&A trade for many years, with a rich history of contributing to this thriving industry. However, a notable trend has emerged over the past decade, wherein India’s growth, especially in apparel exports has been less than stellar. While several factors may have contributed to this stagnation, missed opportunities stand out as a key factor. India possesses immense potential in terms of its skilled workforce, diverse textile offerings, and manufacturing capabilities. Yet, a failure to capitalise on emerging market trends, evolving consumer preferences, and timely investments in modernisation has hindered the country’s ability to fully leverage its position in the global apparel export market.

In contrast to India’s relatively stagnant growth of 4 per cent CAGR in the apparel sector over the past decade, neighboring countries such as Bangladesh and Vietnam have surged ahead with remarkable strides of 10% CAGR each (Data in below graph). These countries have made substantial investments in state-of-the-art manufacturing systems, capitalised on cost-effective labor forces, and implemented strategic government policies to foster industry growth. From the graph, we can understand China’s growth is reduced in global market as the market share of China has also reduced substantially from 43% to 34% over the years 2010 to 2022.

However, the Indian government has shown a strong commitment to revitalising the T&A sector by implementing a range of policies and schemes, which we will delve into in the later part of this article. These initiatives aim to help India regain its competitive edge in every facet of the industry. Simultaneously, Indian manufacturers have embarked on significant endeavors, channeling substantial investments into process control improvements and modernisation. These concerted efforts reflect a shared vision of positioning India as a global leader in the T&A sector.

Indian domestic market has always been resilient, with present market value of US $125bn, it is one of the largest T&A markets in the World. The resilience and vigor of India’s domestic T&A market can be attributed to a combination of factors, each playing a pivotal role in its ascent. Firstly, the rising tide of India’s economy has propelled consumer spending power to new heights. India’s per capita income has been increased by 35% to RS 98,374 in 2022 – 23 from RS 72,805 from 2014 – 15. This increased income has enabled more buying power amongst citizens and thus adversely boosting the economy. Secondly, with a burgeoning young population, the nation is witnessing a surge in the number of fashion-conscious millennials and Gen Z consumers. This shift in consumer demographics has further fueled the dynamism of the domestic T&A market, as it adapts to cater to the unique preferences of these younger generations. Out of India’s total 1.4bn population 55% is under the age of 25 and 65 per cent is under the age of 35. Lastly, the modernisation of lifestyles in India has been a driving force behind the flourishing domestic T&A market. As urbanisation and globalisation continue to reshape Indian cities and towns, consumer preferences have evolved.

Macro-economics factors playing a major role in slowing down of global demand

One of the foremost contributors to the industry’s slowdown was the protracted Russia-Ukraine conflict. This geopolitical tension cast a shadow over the stability of supply chains, affecting the production and distribution of textiles and clothing worldwide. Inflation emerged as another critical factor that played a pivotal role in the industry’s downturn. Rising prices had a domino effect, slowing down consumer demand and curbing imports, particularly in the United States and European Union.

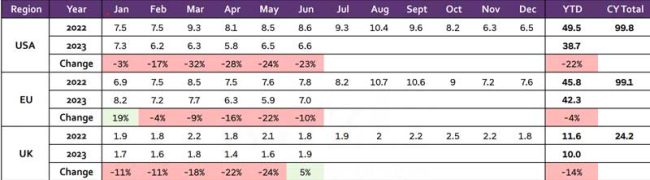

The US and EU, two of the world’s largest textile and apparel markets, experienced reductions in imports. Monthly trade data, (as given below) shows a -22 per cent & -4 per cent YTD decline in apparel imports in USA and EU respectively. These trends reflected the broader economic challenges posed by the aforementioned factors, further exacerbating the industry’s woes.

India, also faced a reduction apparel exports as it is valued $ 1.1 billion, which is 21 per cent lower than in July 2022 exports. On YTD basis, the exports were 15 per cent lower than in 2022. The slowdown in China, India’s major trading partner, had a cascading effect, particularly on India’s cotton and yarn exports. This interdependency highlighted the intricate nature of the global textile supply chain.

Monthly apparel imports of major markets (values in $ billion)

However, amid these headwinds, there is a glimmer of hope on the horizon. We anticipate a recovery in the textile and apparel industry in the near future. The recovery hinges on several factors, including the resolution of geopolitical conflicts, containment of inflation, and the restoration of consumer confidence. As these elements fall into place, the industry is expected to rebound, driven by pent-up demand, renewed consumer spending, and a resurgence in international trade.

Key global trend for 2024

As we look ahead to 2024, the global textile and apparel industry is poised for significant shifts in sourcing dynamics, driven by a convergence of key trends and developments. Following are some of the key trends which will play a major role in dictating the global market dynamics

- Sustainability and traceability: In 2024, sustainability will continue to be a driving force in sourcing dynamics. The industry is embracing emerging sustainable trends and technologies, such as recycled cotton, waterless dyeing processes, and traceability technologies that allow consumers to track the journey of their clothing from raw material to finished product. These advancements are not only reducing the environmental footprint of the industry but also shaping new business models focused on ethical and eco-friendly practices.

- Increasing digitalisation: The textile and apparel industry, like many others, is rapidly digitalising, with this trend accelerating post-COVID-19. From digital design and prototyping to online sourcing and supply chain management, digital technologies are revolutionising the way products are conceived, developed, and manufactured.

- Integrated sourcing: Buyers are increasingly seeking integrated players who can offer end-to-end solutions, from raw materials to finished garments. This trend is driven by the desire for greater efficiency and reduced lead times in a competitive market.

- Consumer trends: Changing consumer preferences are dictating sourcing choices. The demand for comfort wear and activewear, coupled with a growing awareness of sustainability issues, is pushing brands and manufacturers to source materials and produce clothing that align with these trends.

- Shift away from China: China’s share in the global textile and apparel market is gradually decreasing. Countries like Bangladesh and Vietnam are gaining a larger share due to their competitive labour costs and growing manufacturing capabilities. The Xinjiang cotton ban has also impacted China’s cotton apparel exports, prompting buyers to explore alternative sourcing options.

- Raw material price trends: The cost and availability of raw materials, especially cotton, will continue to influence sourcing decisions. Keeping an eye on global cotton production outlook and price trends is essential for industry players to manage costs and secure a stable supply chain.

Opportunity for India

Looking forward to 2024, India finds itself at the crossroads of immense opportunity in the global textile and apparel industry. Several key factors are converging to create a favourable environment for India to not only strengthen its existing presence but also expand its footprint across a broader spectrum of products and services.

- The “China +1” window: With the ever-changing global geo-political scenario global buyers want to de-risk their sourcing strategy and reduce their dependence on a single country. China has been the most dominant supplier of textiles and apparel over the years and will continue to play a significant role in the trade dynamics. However, buyers want to reduce their dependence on China and are looking at other options across categories. India stands to gain from this shift and there is a huge opportunity for India to gain trust of global buyers and make the most out of this opportunity. Attracting foreign direct investments (FDI) to enhance the value chain and infrastructure will be pivotal in capitalising on this window.

- Leveraging PLI (Production-Linked Incentive) & PM MITRA: India’s government initiatives, such as PLI and PM MITRA, offer a strategic pathway to diversify product categories. The global trade potential for synthetic textiles and technical textiles is vast, and India has the opportunity to become a global hub for exports in these domains. Attracting large-scale investments to bolster production and innovation in these segments is critical.

- Diversification in products: India should strategically pivot towards product diversification beyond convention, such as polyester-based textile products and technical textiles to bolster its market share on the global stage. As the world undergoes a transformative shift towards sustainable and innovative materials, India has a golden opportunity to emerge as a key player in these sectors. Polyester-based textiles, with their versatility and eco-friendly variants, can cater to the evolving consumer demands for durable yet environmentally conscious clothing and home textiles. Simultaneously, the pursuit of technical textiles presents avenues for India to leverage its technical prowess in sectors like healthcare, automotive, and construction, etc. By diversifying into the product segments, India will align itself with the changing dynamics of the global textile industry, ensuring a competitive edge in the years to come.

- Free Trade Agreements (FTAs): Recent FTAs signed with countries like Australia and the UAE can be leveraged to boost exports. The potential for new FTAs with the UK, Canada, and the European Union holds the promise of further expanding India’s reach in international markets. While it may be a challenge to establish these FTAs, it will benefit Indian textile and apparel exports if and when they are finalised. Considering China has more than 25% market share in these Markets, India can also aim for at least a 15 per cent market share in these countries. Accordingly, India can add a potential market of $ 15-20 billion through FTAs with these major T&A markets of the world.

- Focus on business excellence: To tap into the global market opportunity, India needs to prioritise several aspects of business excellence. Manufacturing excellence is essential to ensure high-quality, cost-effective production. Sustainability and compliance are increasingly important as consumers demand eco-friendly practices. Digitalisation and a service-oriented approach can enhance efficiency and customer satisfaction. Moreover, investing in product innovation and exploring partnerships with global players and research institutes can open new avenues for market expansion. Partnerships are being explored by competing nations to enhance their capabilities, an example of this is a recently signed MoU between The Korea Federation of Textile Industries (KOFOTI) and the Vietnam Textile and Apparel Association (VITAS) to strengthen bilateral cooperation on issues of sustainable development, digital transformation and supply chain development. India can also explore similar partnerships for new product development and innovations.

In conclusion, the textile and apparel industry is on the cusp of a transformative period in 2024. India is emerging as global power with multiple successes, be it “Chandrayaan -3” or hoisting the global G20 summit. The global giants from other sectors like ‘Apple’, ‘Nvidia’, ‘Tesla’ etc. are looking to build India as their next hotspot for manufacturing and sourcing. Already, we’ve seen several trade discussions of India with established markets like USA, UK, EU etc., highlighting investment and expansion of manufacturing across various segments. For now, India is having a great window of opportunity to capitalise on the market trends. As we anticipate a rebound in market demand, driven by the easing of inflation and a resurgence in consumer consumption, the sector presents exciting opportunities for growth. India’s domestic market, already a significant force, is expected to maintain its momentum.

To capitalise on these opportunities, Indian players must be proactive and adaptive. Aligning their businesses with global trends, understanding buyer preferences, and staying attuned to evolving consumer demands will be pivotal. This era demands innovation, sustainability, and agility. As the industry landscape evolves, India has the potential to not only regain its competitive edge but also emerge as a global leader in the textile and apparel sector. By embracing change, fostering innovation, and staying customer-centric, Indian businesses can navigate the dynamic currents of the industry and secure a prosperous future in 2024 and beyond.

About the author: Dip Naskar is a Consultant at Wazir Advisors.