With modernised infrastructure, government support, and a renewed focus on innovation and market access, the Indian industry is poised to reclaim its global leadership despite recent stumbles, opines Rakesh Mehra.

Textile Industry in India is playing a pivotal role in country’s economy and employment generation, especially for women in the rural areas. With one of the most modernised technological infrastructures in the world and owing to the recent policy announcements such as PLI, PM MITRA, etc coupled with the FTAs which Government of India has signed or negotiating the major T&A markets like Australia, UAE, EU-27, UK, etc., Indian Textile & Apparel Industry is all poised to grow in the years to come.

Current outlook of the global and Indian textile & apparel industry

Global Textile Industry in the past few months has been hit due to various reasons such as the increased inflation, economic slowdown, prolonged Russia-Ukraine war, ongoing Israel Hamas conflict which has resulted in decreased demand of textile & apparel products globally and is thus also impacting the exports of textile & apparel products from India. Data released by the Department of Commerce shows that During April-November 2023, exports of India’s T&A have declined by about 6.58 per cent as compared to Apr-Nov 2022 and about 15.97 per cent as compared to Apr-Nov 2021.

As we are entering into 2024, business conditions are expected to improve and the same is also apprehended in one of the survey’s conducted by the International Textile Manufacturers Federation (ITMF) in November 2023 according to which only 5 per cent of the respondents have reported a major cancellation of 30 per cent of order or more and 44 per cent of the respondents reported that in next 6 months i.e. first half of 2024, business situation for Textile & Apparel Industry will be more favourable and the demand for Textile & Apparel products globally are expected to increase. The same is also being complemented by the increased exports of textile products (excluding apparel) from India during the month of September, October and November 2023 as compared to 2022.

Challenges being faced by Indian T&A Industry

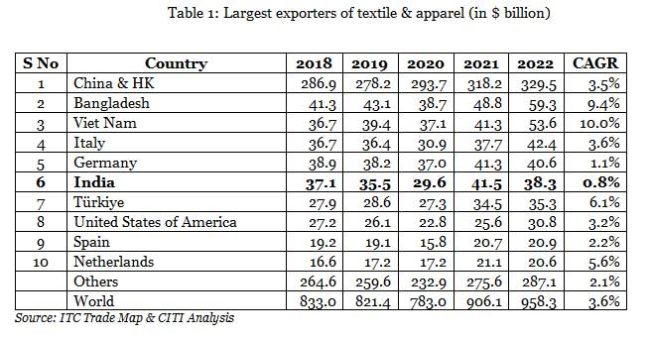

India has one of the most modernised textile industry in the world and the 2nd largest textile manufacturing base in the world. With an estimated market size of about $ 160-170 bn, Indian T&A industry is one the largest in the world. Moreover, India is one of the few countries in the world which have presence of entire Textile Value Chain ranging from fibre to fashion and textile machinery. However, since last few years, Industry is witnessing a stagnation in demand of T&A products domestically as also the export figures are not so encouraging. India, which used to be the 2nd largest exporter of T&A in the world till 2017 has slipped to 6th position in 2022 and was overtaken by countries like Bangladesh and Vietnam which are dependent on imports of raw material for their Textile Industry.

Trade data suggests that during the last 5 years global exports increased at a CAGR of 3.6 per cent during 2018-2022. While countries like Bangladesh and Vietnam have been able to achieve CAGR of 9.4 per cent and 10 per cent respectively, India could achieve a growth of only 0.8 per cent which was also the lowest by any of the top 10 exporters of T&A to the world (see Table 1).

It signifies that amid increasing competitive landscape while countries like China, Bangladesh, Vietnam, etc. have been able to take advantages of lower factor costs & other production costs as compared to India which had made them more cost-effective for buyers. Moreover, Indian T&A industry on the other hand is also facing certain other issues which is hindering its export potential such as:

Non-availability of raw materials at competitive rates: The imposition of 10 per cent duty (5 per cent Basic Customs Duty (BCD) and 5 per cent Agriculture Infrastructure and Development Cess (AIDC)) on Cotton and 10 per cent BCD on Cotton Waste since February 2021 has made it difficult to import cotton at cheaper rates. Further, the levy of import duty has prompted the trade to adopt an import parity pricing policy, making not just the home grown cotton expensive but also other MMF fibres.

The recently announced QCOs have disrupted the availability of raw materials particularly MMF which is leading to surge in imports of downstream products and also increase in fibre prices thus affecting the entire domestic T&A industry. To avoid such disruption it is suggested that the Government may start with QCOs for garments which are left open [for imports] by introducing QCOs for fibre/yarn.. What should be of good quality is what touches the skin. However, garment and fabrics are being imported freely without any QCO The entire textile industry is in for QCOs and good quality, but, it should be introduced first at the garment stage to give direct benefit to the customers.

High volatility in raw material prices: During the last 2 years, Indian T&A industry had been facing challenges of high volatility in raw material prices particularly for cotton. As the spinning mills carry 2 to 3 months of cotton and yarn inventory, it had resulted in the erosion of the working capital of mills which have affected their operational efficiency.

Way forward

Present Government under the dynamic leadership of Hon’ble Prime Minister Shri Narendra Modi is taking slew of measures to support the Indian T&A industry such as:

Production Linked Incentive Scheme and PM MITRA: Aimed at bringing production scale and making global champions of Textiles

Trade agreements with major markets: Government has recently signed the trade agreement with UAE and Australia and many other with major markets like EU, UK, Canada are in pipeline.

While the financial incentives and other benefits under the above and several other scheme will definitely help the Textile Sector in becoming more cost competitive and increase its market share, there are some other suggestions also which industry feels can help the Indian Textile Industry ride over the present crisis such as:

Raw Material Security: Government should ensure that the Indian Textile Industry has access to raw materials of all types at competitive prices as the effect of price increase in raw material multiplies by several times till it reaches the finished goods and thus affect the cost competitiveness of the T&A products.

In this regard, Government may remove the 11per cent duty on cotton imports which have eroded the cost competitiveness of Indian cotton sector and instead of imposing ADD on several raw materials like VFY, Government may encourage Industry to reach to a common consensus where interest of each stakeholder of the value chain is safeguarded.

Moreover, as per the industry estimates, to achieve the requisite market size of $ 350 bn (including $ 100 bn exports), India would need to at-least double its manufacturing capacity of all types of raw materials and also address various other related issues by the below measures:

Initiatives on ESG: ESG norms are slowly becoming a priority for the textile stakeholders, both for business efficiency and for better access to the market. There is a dire need for the industry to define benchmarks related to the reporting framework. Extensive awareness and capacity building programs are also needed in this regard. In this regard, Ministry of Textiles has already formed a ESG task force with an aim to unite the diverse stakeholders – from manufacturers and service providers to waste handlers and innovators – for disseminating knowledge about the ‘Whys, How’s, and What’s’ of ESG, fostering a collective understanding and commitment to sustainable practices. CITI, as a committed member of the ESG Task Force is playing a crucial role in facilitating industry feedback for the various ESG initiatives which Government is planning for the industry along with the practical realisation of the sustainable initiatives. One of CITI’s commitment includes raising awareness and helping the industry towards capacity building related to the ESG requirements within the industry. Towards this CITI has embarked on an awareness series to educate the industry stakeholders about the intricacies of managing, monitoring and reporting on ESG parameters.

Apart from the above, Government may also bring new investment incentivisation schemes to encourage scaling up, innovations, and sustainable technologies such as:

⦠Expediate finalisation of Alternate Scheme to Technology Upgradation Fund Scheme (TUFS)

⦠Early announcement of PLI 2.0 with lower investment threshold and wider products coverage

With modernised infrastructure, government support, and a renewed focus on innovation and market access, the Indian industry is poised to reclaim its global leadership despite recent stumbles. The industry’s trajectory in 2024 hinges on robust implementation of initiatives, sustained technological adoption, and a proactive stance toward addressing critical issues. Navigating these dynamics by weaving together talent, technology, and sustainability, India’s T&A sector holds the potential to become a global powerhouse, creating a brighter future for its people and its economy.

About the author:

Rakesh Mehra is a Chairman of Confederation Of Indian Textile Industry (CITI) , and is also the Chairman of Banswara Syntex (BSL), an integrated textile manufacturer & exporter of yarns, fabrics, and garments, having a turnover of Rs 1,400 crores. He is a Chartered Accountant and has has been associated with various Industry Associations. He was elected Chairman of The Synthetic & Rayon Textile Export Promotion Council (SRTEPC) for two terms. He was President of Indian Spinners’ Association (ISA), and Deputy Chairman of the Confederation of Indian Textile Industry (CITI).