The Indian textile & apparel industry witnessed a significant recovery in terms of overall sales and EBITDA levels in H1 FY22. The value of Indian export has drastically improved, says Sanjay Arora.

The Indian textile & apparel industry (WTI) encompasses the highlights of the cumulative financial performance of the top Indian textile companies concerning the market performance of the Indian textile sector for H1 FY22.

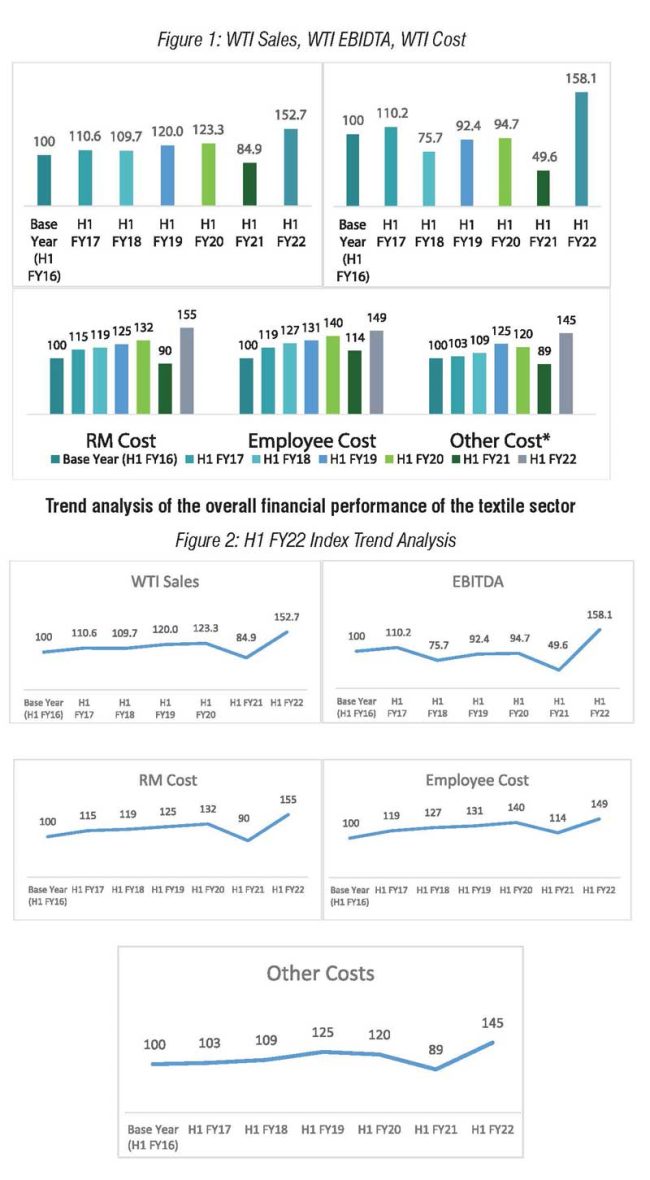

Eased covid restrictions have resulted in the re-opening of manufacturing units across the country and the emotion of revenge shopping has resulted in a significant recovery in sales and profitability of the companies. WTI Sales was calculated to be 152.7 in H1 FY22 (Base, H1 FY16=100), which has significantly overshadowed the sales of 123.3 seen in H1 FY20. The WTI EBITDA was calculated to be 158.1 in H1 FY22 showing a drastic gain of 67% from the values of 94.7 in H1 FY20. The WTI Cost for raw material (RM), employee, and other expenses were 155, 149, and 145 respectively, in H1 FY22.

The consolidated sales of the selected top 10 companies are Rs. 24,024 crores in H1 FY22 which has grown at a CAGR of 11% from Rs. 19,400 crores in H1 FY20. As compared to H1 FY20, the average EBITDA margin has also raised by 5.0 percentage points in H1 FY22 for the selected top companies. Average RM cost decreased by 4.0 percentage points, while the average employee cost decreased by 1.0 percentage points in H1 FY22 as compared to the H1 FY20.

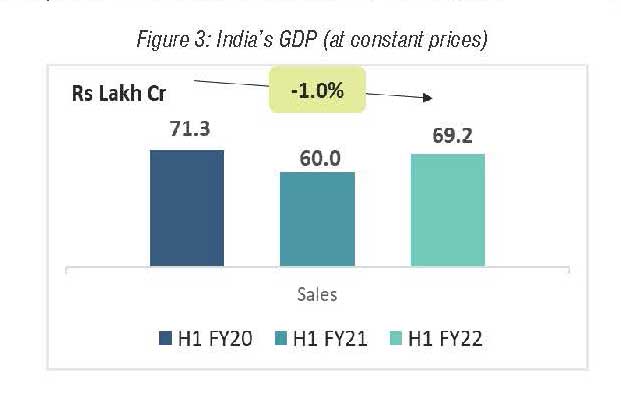

India’s GDP declined by 1% in H1 FY22 when compared to H1 FY20

India’s Gross Domestic Product (GDP) is estimated at Rs. 69.2 lakh crores in H1 FY22, as against Rs. 71.3 lakh crores in H1 FY20, witnessing a decline of 1%. The estimated GDP has recovered by 15.4% when compared to covid hit GDP at Rs. 60.0 lakh crores in H1 FY21.

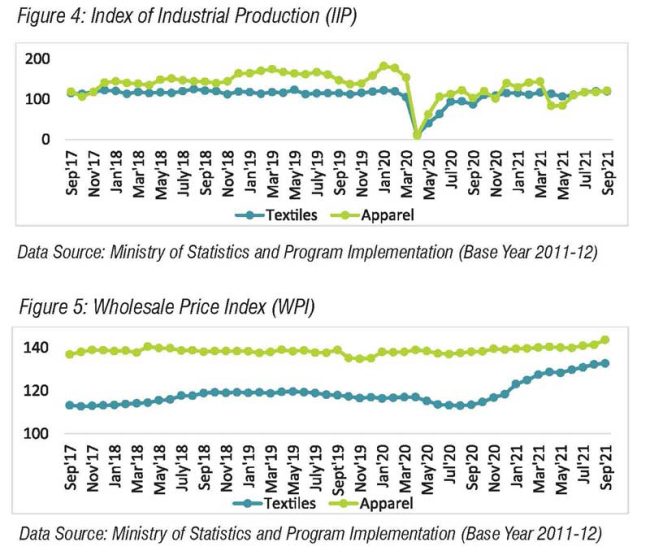

The average Index of Industrial Production (IIP) for apparel decreased by 34% in H1 FY22 when compared to H1 FY20, while that of textiles has rebounded to the levels seen in H1 FY20. In H1 FY22, the Wholesale Price Index (WPI) for textiles increased by 5%, while that of apparel increased by 1% when compared to H1 FY20.

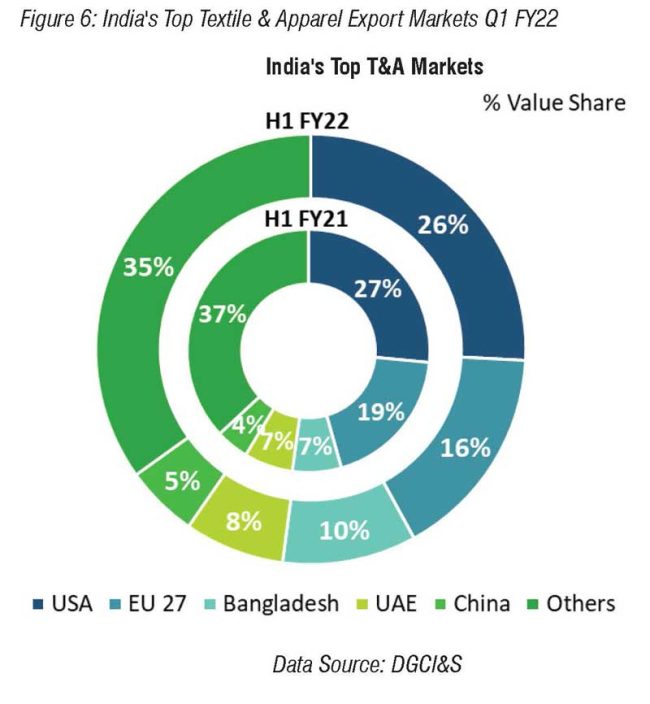

The textile and apparel exports of India have recovered in H1 FY22

The textile & apparel exports in H1 FY22 stood at US$ 20.38 billion, growing at a CAGR of 10% since H1 FY20. The exports of fiber and yarn have witnessed the highest CAGR of 63% and 35%, respectively in H1 FY22 since the exports witnessed in H1 FY20. USA, EU-28, and Bangladesh remain the top export destinations for India’s T&A products with a combined share of 52%.

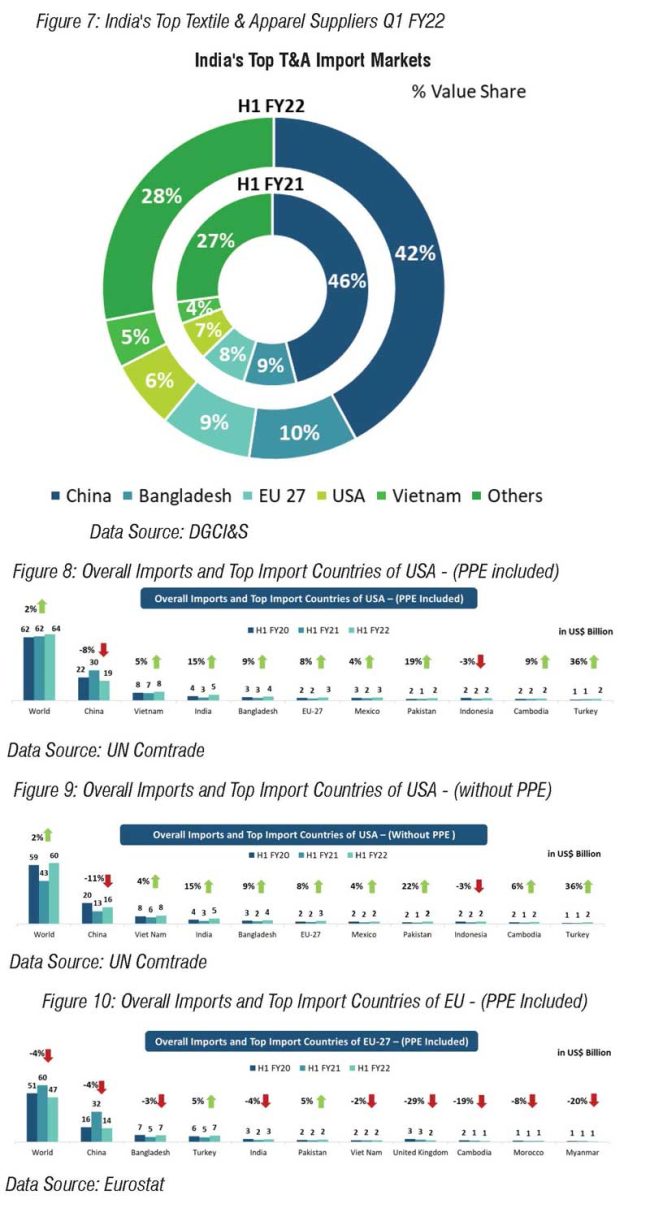

The textile and apparel Imports of India has declined in H1 FY22

India’s textile & apparel imports stood at $ 3.76 billion in H1 FY22, recording a decline rate of 10% since H1 FY20. The imports of fiber and home textiles experienced the highest decline rate of 31% and 20%, respectively in H1 FY22 when compared to the imports in H1 FY20. The imports of MMF yarn are on a rise and have grown at a CAGR of 18% in H1 FY22 since H1 FY20.

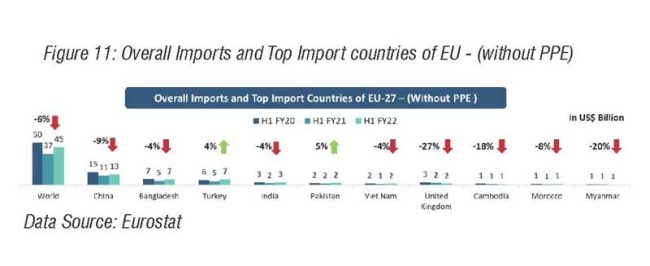

Textile & Apparel imports of USA has grown at the rate of 2% in H1 FY22 (excl. PPE imports)

USA imported textile & apparel products worth US$ 64 billion in H1 FY22, out of which US$ 4 billion was PPE imports. Excluding PPE, in H1 FY22 the imports witnessed a CAGR of 2% when compared to that in H1 FY20. The share of India’s exports to the USA has increased at the CAGR rate of 15% from H1 FY20 to H1 FY22.

Textile & apparel imports of EU declined at the rate of 4% in H1 FY22* (excl. PPE imports)

With a value of US$ 47 billion in H1 FY22, since covid has hit the countries multiple times the overall textile & apparel imports of the EU have declined at the CAGR of 4% since H1 FY20. The market for India’s exports to the EU in H1 FY22 has declined at the CAGR of 4% since H1 FY20. Imports from Pakistan are on the rise.

India’s Scenario

India’s exports to the USA stood at US$ 5.0 billion in H1 FY22, showing a steady growth of 15% when compared to the H1 FY20. For the EU, India’s exports stood at US$ 2.8 billion in H1 FY22, showing a decline of 4.0% over US$ 3.1 billion in H1 FY20. The share of Chinese T&A exports to EU-27 have declined at the CAGR rate of 4% from H1 FY20 to H1 FY22 and the same trend has been witnessed for the USA at the rate of 8%.

The Indian textile & apparel industry witnessed a significant recovery in terms of overall sales and

EBITDA levels in H1 FY22. The value of Indian export has drastically improved. The China+1 sentiment is playing a pivotal role in the raging recovery of the Indian textile industry. The scope of becoming an alternate manufacturing hub in the international export market is immense and the Indian textile industry looks poised to captivate on the opportunity.

About the author:

Sanjay Arora is the Business Diretor of Wazir Advisors. He is a certified Internal Auditor QMS – ISO 9001-2000 with 24 years of experience in business consulting, operational excellence, government advisory services, customer relationship management, production planning, process improvement and project management across the textile industry. Sanjay Arora has worked with premier textile and polyester manufacturing industry in India at various levels. He has been a speaker at various national and international textile & apparel conferences/seminars e.g. CCI, CII, FICCI, TAI, etc. He can be reached on Email: sanjay@wazir.in

Images Source: Google Images