The current market situation faces headwinds manifested in key macroeconomic trends such as inflation, soaring energy prices, continued effects of the coronavirus and the prolonged war in Ukraine. In this article, Navdeep S Sodhi captures the current state of the textile economy and recapitulates the long-term trends in the light of the current macroeconomic conditions.

The annual ITMF (International Textile Manufacturers Federation) conference was held in September after a hiatus of two years in the Alpine Mountain resort of Davos. The Swiss town is better known for the World Economic Forum (WEF) that takes place in winter. However, the proceedings at the ITMF were equally important to deliberate on the situation in the $2 trillion global textile and clothing economy. Interestingly, if textiles were to be a country it would rank as the 10th largest economy, a step ahead of Italy in terms of GDP.

This article captures the current state of the textile economy and recapitulates the long-term trends in the light of the current macroeconomic conditions.

World economy and the textile and clothing demand

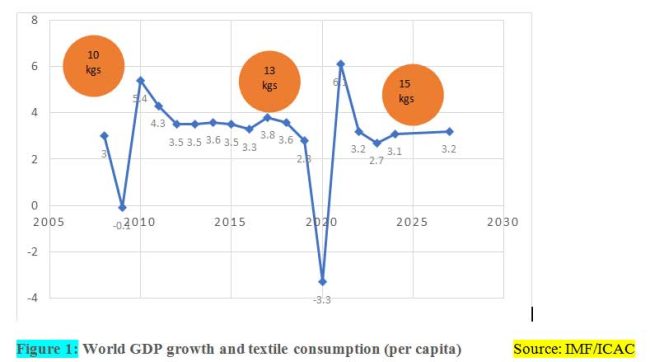

2021 marked the recovery of the apparel demand. The revenue of top 11 fashion brands and retailers reached $ 107 billion, a 20 per cent increase from the nadir in 2020 and exceeding the 2019 retail sales of $ 102 billion. The global trade in textiles and clothing in 2021 was $ 785 billion, yet below the previous peak of 2019 ($ 807 billion). Textile consumption has an axiomatic relationship with GDP. Figure 1 shows the correlation between GDP growth and per capita textile consumption. Textile consumption per capita is projected to increase to 15 kgs by 2027 as the world economic growth recovers.

The current market situation faces headwinds manifested in key macroeconomic trends such as inflation, soaring energy prices, continued effects of the coronavirus and the prolonged war in Ukraine. In a recent blog the IMF’s Kristalina Georgieva, Gita Gopinath and Ceyle Pazarbasioglu spoke of a “confluence of calamitiesâ€: including Ukraine and the pandemic which pose a grave risk to the world economy. The world economic growth has slowed and accordingly to the latest forecasts, the world economic growth in 2022 and 2023 will halve compared to 2021.

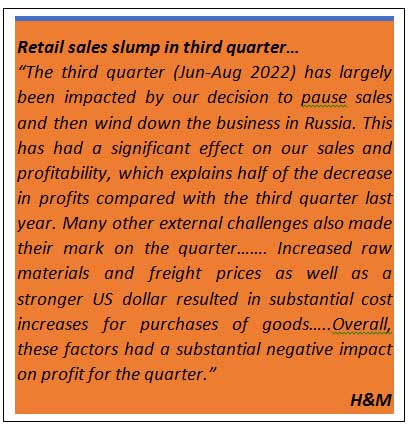

International fashion retailers have reported rise in inventory and pressure on their margins since summer. This is also reflected in the slump in their offtake from supplying countries.

World economic outlook

As per the World Economic Outlook, released by IMF on October 11, 2022, “Global growth is forecast to slow from 6.0 percent in 2021 to 3.2 percent in 2022 and 2.7 percent in 2023. This is the weakest growth profile since 2001 except for the global financial crisis and the acute phase of the COVID-19 pandemic and reflects significant slowdowns for the largest economies: a US GDP contraction in the first half of 2022, a euro area contraction in the second half of 2022, and prolonged COVID-19 outbreaks and lockdowns in China with a growing property sector crisis.â€

The growth forecast for India has been revised downwards to 6.8 per cent for 2022 and 6.1 per cent in 2023 (2021: 8.7 per cent).

Inflation

Central Banks around the world are struggling to tame stubbornly high inflation in double digits since 1980S. The two root causes of the persistent inflation were unprecedented government spending on stimulus (totalling 10 per cent of global GDP), loosening funds into the economy and the supply chain disruptions in the wake of the pandemic. To these twin factors was added the energy crisis since the Ukraine war since February.

US Federal Reserve has adopted the most aggressive approach by raising the interest rates to 3.25 per cent from close to zero at the beginning of the year. It is predicted that the US interest rates will hit 4.5 per cent, the highest since the financial crisis in 2008. The Bank of England raised interest rate to 2.25 per cent, the highest since the financial crisis. Even Switzerland and Japan were compelled to deviate from their negative interest stance held for a long time. The markets are predicting that by June 2023, the policy rates in advanced economies will be even higher in 2023. The tight monetary policy is having an adverse effect on developing countries in Asia which have been forced to raise interest rates to reign in the impact of high cost of energy and falling currencies. It is apparent that, in the short term, we will have to get used to new normal of higher inflation as governments may have to keep spending on public projects to keep the economy on steroids.

Exchange rates

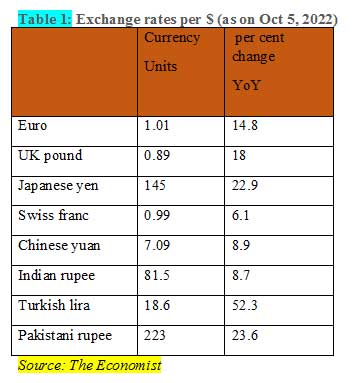

The strength of the greenback has led to a turmoil in the currency markets. It has affected the currencies of the advanced and the emerging markets alike. The Chinese yuan and Indian rupee have declined about 9 per cent.

Energy crisis

The void created by curbs on energy exports by Russia is leading to an energy crisis for developing countries, especially in the Indian sub-continent. Because of high demand for LNG in Europe, the sub-continent is facing an energy crunch. Pakistan and Bangladesh are facing acute power shortages. The natural gas scarcity is also forcing these countries to turn to dirtier fuels like coal. According to Wood McKenzie, small industries in India are switching to fuel oil and LPG for heating while oil-fired power generation has surged 5-fold in Pakistan and 45 per cent in Bangladesh.

The surge in energy cost and fears of power shortages are severely affecting household incomes and industrial output in EU. Germany, Europe’s largest economy, has responded with the announcement of a Euro 200-billion energy packages to insulate its consumers and industry.

In India, as per the administered price mechanism (APM), the price of natural gas was raised 40 per cent to $8.57 per mBtu for the second half of the current FY with effect from October 1, 2022.

Trade growth to sharply slowdown in 2023

According to the latest press release from the WTO, the world merchandise trade is expected to lose momentum in the second half of 2022 and remain subdued in 2023 as multiple shocks weigh on the global economy. WTO economists now predict global merchandise trade volumes will grow by 3.5 per cent in 2022. For 2023, however, they foresee a 1.0 per cent increase—down sharply from the previous estimate of 3.4 per cent. Import demand will slow down in advanced as well as emerging economies. In the US, the housing demand will be affected by the high mortgage rates whereas in EU the disposal income will shrink due to rising energy bills. The developing countries will also feel the impact of high food and energy inflation and reduction in disposable income. The WTO forecasts that the growth of merchandise imports in North America will decline to 0.8 per cent in 2023 compared to 8.5 per cent 2022 whereas Europe’s imports are forecast to show a negative growth of – 1.0 per cent against 5.9 per cent growth in 2022.

Impact on the textile economy

Changes taking place around the world would impact the textile industry in various ways.

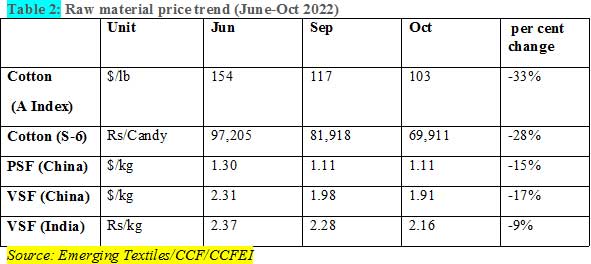

Raw materials: The prices of all textiles raw materials have declined in the recent months in response to the weak market sentiment and reduced offtake by spinners and downstream industry. Cotton experienced the most volatility; however, prices of feedstock and man-made fibres were not immune to the trend. Cotton prices on international and domestic markets have been declining significantly since September as a reflection of the market sentiment. The A-index fell 18 per cent; however, it was the Indian cotton prices that plummeted 30 per cent. The USDA October report has cut the forecast for consumption to 25.1 million tonnes – the lowest in recent five years (barring the pandemic year 2020/21) – leading to high closing stocks in 2022/23 season.

Prices of man-made fibres have also dropped significantly. PSF prices in India declined from a peak of Rs 128/kg in June to Rs 107/kg in October (13 per cent); Chinese PSF prices too fell by 7 per cent from a peak of $1.30/kg to 1.11/kg in October. The prices of feedstock have also declined in the last three months in tandem with fall in crude oil prices. The price of PTA declined from a peak of $1082/tonne in June to $874/tonne in October; MEG price in spot market dropped from $613 to $495/tonne in the same period.

Price of VSF in China and India declined significantly. The price of DWP (dissolved wood pulp) – the raw material for VSF – dropped from $1200/tonne in July to $1061/tonne in October.

Trade: The first signs of slowdown are evident from the lower growth rate of US apparel imports. According to the latest data from OTEXA, in August, US imports of apparel rose by 7.6 per cent compared to a YoY increase of 17.6 per cent in the previous month. This reflects the slowdown in retail sales in the US. Imports from China and Vietnam dropped by 6 per cent in volume term although there was still an increase in value terms.

Sourcing shifts

International trade in textiles and apparel is characterised by sourcing shifts. While the gradual long-term shifts are consistent with the nature of our itinerant industry, the trends have accelerated in recent years. The buyers are extremely concerned about geo-political factors, risks of over-dependence on a single country and high cost of logistics. A closer look at the sourcing of apparel by the US and EU manifests these trends.

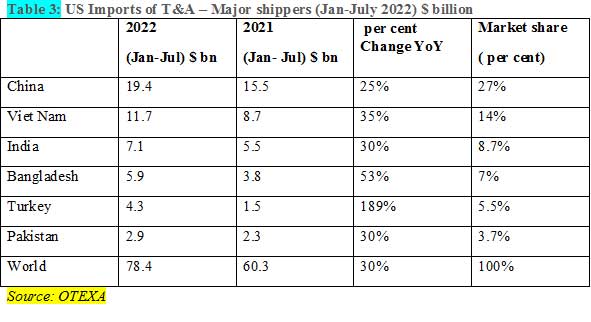

During the first half of 2022, the US imports of textiles and apparel were $78.4 billion, a 30 per cent increase over the corresponding period in 2021. China remains the largest supplier; however, Vietnam and Bangladesh were the major beneficiaries of the 30 per cent increase in the US imports. Imports from Turkey jumped 189 per cent indicating that it will become a key player in the US market in coming years.

West Africa emerging as a new sourcing hub

Frontier markets that are emerging because of the strong interest from the international buyers to diversify their sourcing strategy. This phenomenon has been evident in CIS and Africa.

Arise IIP an industrial park developer from UAE is setting up a mega integrated textile and garment complex in West Africa. Two industrial parks are being set up in Benin and Togo, in the West African cotton belt. Notably, the Francophone West Africa produces about 2/3rd of Africa’s cotton (1.4 million tonnes) most of which is presently exported. GDIZ and PIA industrial parks aim to reverse this trend and transform cotton into finished garments for exports.

Sub Saharan African countries enjoy duty-free preferential market access to the US and EU, besides the regional ECOWAS market of over 400 million consumers. The textile and garment projects will be equipped with state-of-the-art machinery from world renowned suppliers and meet the highest sustainability standards demanded by international buyers. These include sustainably certified and traceable cotton, renewable energy and ZLD. Being located in close proximity to ports, the Arise textile parks will enjoy logistical advantages and speed to market. The projects carry strong government support in terms of fiscal and concessional tariffs for utilities.

The textile and garment industry in the region is receiving strong policy and financial support from international institutions. World Bank Group through its private sector lending arm the International Finance Corporation (IFC) is supporting viable textile projects in the region. On the other hand, the Tony Blair Institute for Global Change and the UK government’s international development arm FCDO (Foreign, Commonwealth and Development Office) have been assisting the regional governments in formulating policies to attract FDI in the sector. An international investor summit will be held in Abidjan in November to showcase the opportunities for trade and investment in the T&A industry. West African countries such as Benin, Ghana, Ivory Coast and Togo have been proactive in attracting FDI in the sector. Nigeria which had Africa’s largest textile industry after Egypt is also striving to revive its moribund industry. A high-level delegation from the Industry & Trade ministry visited India in September to explore linkages in investment, trade and capacity building. Gherzi, the renowned Swiss textile advisory, has been partnering with the institutions and industry to grow the regional cotton-textile and garment industry.

Morocco, in northern Africa has emerged as the flagship country to attract investments in circular textile manufacturing. Inditex, the world’s largest clothing retailer, is investing in developing the circular supply chain in the region. Kenya, which is sub–Saharan Africa’s largest exporter of apparel under AGOA, is attracting further investment particularly in the CMT factories exporting MMF apparel.

The emerging Central Asia

The Central Asian region produces about 1.5 million tonnes of cotton with high yield (800 kgs/ha). Uzbekistan, the flagship country in the region has achieved remarkable success in transforming its cotton-textile industry. It has installed about 3 million ring spindles in the last ten years. From being an exporter of cotton, it currently transforms the entire output and is now contemplating investment in production of man-made fibres to diversify the value chain.

Circular textile economy

Reuse is a key aspect of sustainability. The linear business model using virgin materials and generating waste is unsustainable in the long run. According to a study carried out by Gherzi for Euratex. More than 80 per cent of collected textile waste is being incinerated or landfilled. Furthermore, textile- to- textile recycling rate at below 1 per cent presents a major challenge as well as an opportunity.

On the demand side, the commitments made by international brands and retail to incorporate sustainable fibres in general, and end of life recycled fibres into fashion design, give a clear impetus.

With abundant availability of pre- and post-consumer textile waste, India offers tremendous opportunities to international brands and retailers to source sustainable apparels. The existence of well-developed integrated hubs at Panipat and Tiruppur, indigenous machinery manufacturing capability and initiatives of leading textile mills, the textile recycling industry is set for growth.

The last word

It is apparent that the textile industry is not immune to the economic headwinds. The retardation in the world economy in the second half of 2022 and well into 2023 will impact textile consumption significantly. This will pose a major challenge to the industry already in the throes of restructuring and consolidation. At the same time, there are opportunities to align your business models to shifts in sourcing, circularity and digitalization. This is the time to revisit your strategy and reposition for the future.

Navdeep Singh Sodhi, CText FTI, is a Partner at Gherzi Textil Organisation, Switzerland, and Fellow of the Textile Institute Manchester.