Technical Textile: Needs Performance Push

Despite strong demand and policy support, Indian companies largely stay in mid-value technical textiles due to the high risk, cost and long R&D cycles involved in high-performance products. To move up the value chain, Divya Shetty writes how the industry must significantly strengthen its R&D focus.

India today occupies a paradoxical position in the global technical textiles value chain. While domestic demand is robust and policy support has intensified, the country continues to trail global leaders in high-performance segments. The real test lies in whether Indian manufacturers can move beyond commodity and mid-value products into advanced materials that define competitiveness in defence, aerospace, mobility and healthcare.

India has advanced meaningfully in the conversion and application segments of technical textiles, but remains structurally weak in upstream raw materials and critical intermediates across most high-performance categories. Its core strengths are concentrated in downstream manufacturing—from yarn-to-fabric conversion to protective apparel, industrial and coated or laminated textiles, PPE and engineered products—much of which is built on imported high-performance fibres.

According to Nandan Kumar, Managing Director, High Performance Textiles & Institute of Technical Textiles, “Application engineering capabilities are steadily improving, with Indian companies increasingly focusing on product design, prototyping, and value-added solutions such as cut and heat protection, antistatic systems, technical composites, and specialty fabrics. Despite this progress, India continues to be import-dependent for high-performance fibres including para- and meta-aramids, aerospace-grade carbon fibres, high-tenacity specialty fibres, and several functional fibre variants.”

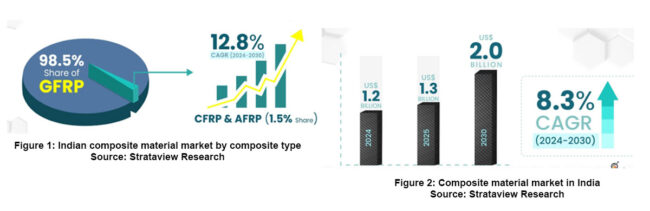

Significant gaps also remain across the composites ecosystem, especially in specialty resins, prepregs, advanced reinforcements and the process expertise needed for defence- and aerospace-grade applications. Similar weaknesses are evident in the carbon-fibre supply chain, where key inputs such as precursors, consistent fibre quality and compatible sizing systems continue to be largely import-dependent. While glass fibre dominates in India with glass fibre reinforced polymers (GFRPs), carbon fibre and aramid fibre follow. The remaining ~2 per cent share (by volume) in the Indian composite material market is held by Carbon Fibre-Reinforced Polymers (CFRPs) and Aramid Fibre-Reinforced Polymers (AFRPs) (see Figure 1).

Paresh Thumar, Director, Zoom Texturisers, discusses how restrictions on raw materials are hindering manufacturing operations. He says, “We do not have enough raw material inputs for new development and for creating new product ranges. All these restrictions are preventing the industry from developing and researching new products to meet local demand. We need to rely on raw materials, not finished products. Our local demand is huge, and I am confident our manufacturing capacity could double or more if there were no restrictions on imports or if the best raw materials were readily available locally for the industry.”

“We are largely import dependent on para aramid fibres, which are used significantly for ballistic, industrial and speciality uses. India is fastest growing buyer of these fibres and supply is dominated by global producers namely – Hoysung, Teijin, DuPont and the likes. Similarly, carbon fibre is relied on imports from USA, Europe, Japan, Korea,” notes Avinash Misar, Director, Texport Syndicate and Past Chairman, ITTA.

High-performance resin systems and specialty chemicals—such as advanced epoxies, prepregs and high-temperature resins—are critical inputs, and their limited availability constrains the performance and certification of advanced composite systems.

India currently occupies a balanced position in the global textile value chain. While the country has strong expertise and execution capabilities in traditional textiles, it is steadily progressing toward the development of downstream, high-performance products. To accelerate this transition, sustained investment across the value chain is essential, opines, Puspen Maity, CEO, Technosport. He adds, “The industry should prioritize applied research and development at advanced Technology Readiness Levels (TRL 7, 8, 9) directly on the production floor, while closely aligning these efforts with market needs, marketing strategy, and consumer insights.”

Where India stands & why it’s stuck

Indian manufacturers continue to focus largely on commodity and mid-value technical textiles, primarily due to barriers related to technology access and intellectual property (IP).

“Para aramids, carbon fibre, all require proprietary polymer chemistry, processed control, know-how, patents and all this are controlled by the global leaders through IP by protecting through IP the trade secrets, processes, supplier lock ins,” informs Misar.

In this context, despite the ability of Indian firms to replicate certain processes, the industry has struggled to advance and mature in upstream manufacturing of specialty fibres. At the same time, licensing critical technologies from established global players—where available—remains prohibitively expensive.

Dr Kumar believes that high-performance textiles typically require extended R&D and validation timelines, including multiple design iterations, bulk trials, field testing, and customer or regulatory approvals, which increase both cost and risk. Progress is further constrained by gaps in testing and certification, as access to certain global standard methods, accredited facilities, and application-specific validation protocols remains limited within the country.

He suggests that a key enabler for accelerating commercialization would be deeper, more structured collaboration with academic institutions, including greater academic participation in bulk-scale trials—such as producing 100 metres of fabric or 100 kg of fibre or yarn—which would allow laboratory research to translate more effectively into industry-ready, commercially viable products in India.

SMEs and MSMEs, which serve as the backbone of the industry, must be provided with the support they need, says Thumar. He adds, “Our SME/MSME sector has strong skills, but we are limiting them by restricting imports and access to global materials. If we want to supply to the global market, we must have the materials that the world demands. We cannot force them to use our local materials if they are not acceptable or suitable. We must offer what they need.”

Industry understanding of application-specific performance is steadily strengthening. Continued progress will benefit from a supportive, market-oriented environment and streamlined policy frameworks. “Simplifying access to NTTM funding can play an important role. A more effective approach could involve the government proactively identifying high-potential enterprises and encouraging R&D investment through revenue-linked incentives, while minimizing administrative complexity,” tells Maity.

Ecosystem & policy reality check

The technical textiles ecosystem is expanding, but its full potential has yet to be realized due to limited visibility. “Currently, a unified platform that provides comprehensive information on available facilities, their locations, and associated costs, will be helpful to the ecosystem. Establishing a centralized, standardized digital portal for testing and R&D infrastructure would also significantly improve accessibility, transparency, and utilization across the sector,” says Maity.

Few industry experts say that the leading companies are creating hurdles such as BIS regulations and anti-dumping duties, which prevent access to the best raw materials for new development and sustainable manufacturing. This is significantly slowing industry growth and expansion. Raw material is the key and backbone of the industry, and it should not be restricted. Otherwise, the manufacturing sector may decline and eventually stop.

However, Dr Kumar informs that awareness of global standards and certification pathways is increasing, yet the ability to conduct meaningful pilot and bulk-scale trials—such as processing batches of around 100 kg to demonstrate consistency and manufacturability—remains a major bottleneck.

Equally vital is a stronger end-to-end validation ecosystem, with faster access to accredited testing, simulations and certification support. Tighter industry–lab integration and quicker feedback loops are essential to cut development timelines and speed up commercialisation of high-performance technical textiles in India.

To sustain and accelerate the momentum in technical textiles, the government has launched initiatives such as the PLI scheme and the National Technical Textiles Mission (NTTM). Dr Kumar sheds some light on what specifically the sector needs as he says, “India’s movement up the value chain will accelerate meaningfully only if these schemes are complemented by a sharper, dedicated push for high-performance fibre and advanced material manufacturing. What is now required is a targeted “advanced materials” mission-mode approach, with focused incentives and time-bound programs for high-performance fibres such as aramids, carbon fibres, and specialty flame-retardant and antistatic fibres, along with advanced resins and intermediates, prepregs and composite systems, and specialty nonwovens and filtration media.”

While larger companies are benefiting from government policies, Thumar calls for SME- and MSME-friendly schemes that would better support smaller players. He comments, “Yes, these initiatives will help encourage investments. However, if they focus more on the SME sector, the impact will be much greater. SMEs/MSMEs outnumber large companies, and if a product is produced by SMEs, it can reach more end-users quickly. If the same product is produced only by large MNCs, it may not be economically viable or affordable for the majority of Indian citizens. The unavailability of raw materials and restrictions on importing them into India remain major challenges.”

Moving up the curve

Finally, for India to compete in high-value technical textiles, a forward-looking strategy rooted in capability building and a mission-driven mindset is essential—anchored in deep technology partnerships and backward integration into fibres, precursors and resin systems. Over the next decade, this will require a structural reality. The focus will have to be break IP barriers, enable execution, de risk investment and sustain long cycles. Our competence to produce industrial plus defence grade carbon fibre, para aramid with global certification and exporting these materials globally would be the final success. The composite material market which is just $1.3 billion now, is said to be double in the next five years (see Figure 2). “The focus will have to be break IP barriers, enable execution, de risk investment and sustain long cycles. Our competence to produce industrial plus defence grade carbon fibre, para aramid with global certification and exporting these materials globally would be the final success,” states Misar.

“Academic and institutional laboratories must also evolve beyond small laboratory experiments to support meaningful bulk-scale trials in the range of 100–200 kg, enabling realistic validation of consistency and manufacturability. In parallel, students should be encouraged not only to develop new materials and products, but also to commercialise them through startup-oriented models during their university years,” states Dr Kumar.

High-performance fibres and advanced materials should be introduced from the first year of textile and material-science education, with companies actively involved in processing these materials participating in lectures, demonstrations, and hands-on training at leading textile institutes.

Thumar recommends, “We need to promote products that can be used in daily life, developed by the young generation through their studies and R&D efforts. The Government of India should act as a PPP partner for newly developed products to scale them up for mass production. This can be achieved with support from government initiatives, banking finance, and consumer-based adoption.”

Global competitiveness will hinge on how effectively Indian manufacturers embed themselves within international innovation ecosystems. Strategic technology partnerships can fast-track capability building, while focused skill development will be vital to sustaining long-term progress. “Rather than viewing competition in isolation, India should actively engage with global markets and collaborators across Asia, Europe, and North America. Our strengths in manufacturing agility, engineering talent, and a growing domestic demand base provide a strong platform for scale. With consistent policy execution and deeper industry–government collaboration, India has the potential to establish itself as a credible and trusted player in high-value technical textiles,” concludes Maity.

Backed by global collaborations in co-development of composite materials, joint validation and research publications—and reinforced by shared pilot facilities and faster pilot-to-commercial pathways—these measures can significantly accelerate India’s transition towards globally competitive, high-value technical textile manufacturing.

QUOTES:

- High-performance fibres need pilot plants, long gestation funding and mission-driven risk sharing—conditions the current investment ecosystem struggles to support.

- Avinash Misar, Director, Texport Syndicate and Past Chairman, ITTA

- India’s strengths lie in downstream technical textiles, but high-performance fibres and critical intermediates remain largely import-dependent

- Nandan Kumar, Managing Director, High Performance Textiles & Institute of Technical Textiles

- SMEs are the real growth engine, and policies must enable them if new technical textile products are to reach the market at scale.

- Paresh Thumar, Director, Zoom Texturisers

- Applied R&D at the production floor—rather than the laboratory—will be critical to building globally competitive technical textiles.

- Puspen Maity, CEO, Technosport