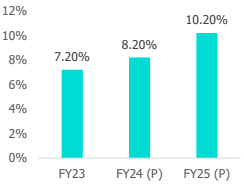

The Indian polyester yarn industry is expected to witness around 100 bps improvement in PBILDT margin during FY24 over FY23.

During CY22 (CY refers to the period from January 01 to December 31), out of global fibre production of 116 million tonne, polyester fibre accounted for a lion’s share of 54 per cent, with the production of 63 million tonne. In the global polyester yarn industry, China, the largest player, is 6-8 times in size than the second largest player i.e., India.

Cheap import of polyester yarn from China

Leveraging its access to cheaper Purified Terephthalic Acid (PTA), China not only dominates the export market but also fulfills the demand of its large export-oriented textile and apparel industry. India can manufacture 4.5-5 million tonne of polyester yarn annually and consumes over 80 per cent of it domestically.

The zero-COVID policy implemented by China during FY23 significantly impacted its domestic consumption of textile products. Despite the Chinese economy not recovering at the anticipated pace after the opening-up of its economy, Chinese manufacturers did not curtail production in line with the slowdown in domestic demand. Instead, they started dumping polyester yarn at cheaper rates in the global markets. Consequently, there was a significant increase in Chinese imports to India during FY23 which persisted into H1FY24 as well. This not only adversely impacted the pricing power of Indian manufacturers in the domestic market but also led to a contraction in their

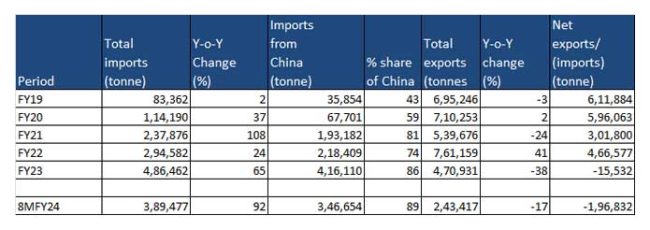

Table 1: Total imports of China

Source: CMIE; Compiled by CareEdge Ratings

During FY23, imports of polyester yarn surged by 65 per cent on a year-on-year basis, while exports experienced a decline of 38 per cent year-on-year. Consequently, Indian polyester yarn exports hit a decade-low level in FY23, in stark contrast to the decade-high level of imports during the same period. This resulted in a significant oversupply in the domestic market in FY23 over FY22, impacting the sales realisation of industry players (see Table 2).

During FY23, India became a net importer of polyester yarn for the first time in the last decade, which continued during 8MFY24 as well. Despite largely stable sales volume supported by robust domestic demand, the PBILDT margin of polyester yarn players was significantly impacted due to competitive pressure on average sales realisation to maintain capacity utilisation to counter cheaper Chinese imports.

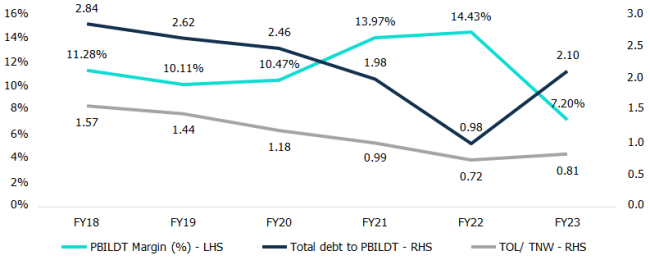

Table 2: Moderation in profitability and debt coverage indicators of Indian polyester yarn players

Source: Annual Reports of 13 companies commanding over 65% of market share; compiled by CareEdge Ratings

The operating profitability of Indian polyester yarn players had witnessed significant improvement during FY21 and FY22 backed by healthy growth in sales volume and an increase in average sales realisation aided by the industry upcycle. The moderation in PBILDT margin during FY23 was mainly due to the influx of cheaper polyester yarn imports, resulting in a decline in average sales realisation.

With the accretion of strong profitability during FY21 and FY22, industry players reduced their reliance on external liabilities. Consequently, the capital structure marked by TOL/TNW improved and remained comfortable at 0.81x as of March 31, 2023. However, total debt to PBILDT which had improved gradually from 2.84x during FY18 to 0.98x during FY22, witnessed a moderation in FY23 due to subdued profitability. However, it continued to remain better than its historical level supported by debt reduction done by industry players during FY21 and FY22.

Implementation of QCO on polyester yarn

The Government of India (GoI) implemented QCO on polyester yarn which mainly includes fully drawn yarn (FDY) and partially oriented yarn (POY) to establish quality standards and restrict the import of inferior products. The Bureau of Indian Standards (BIS) plays a crucial role in ensuring compliance with the quality standards set in the QCO by certifying products that meet the prescribed standards for both domestic and international manufacturers.

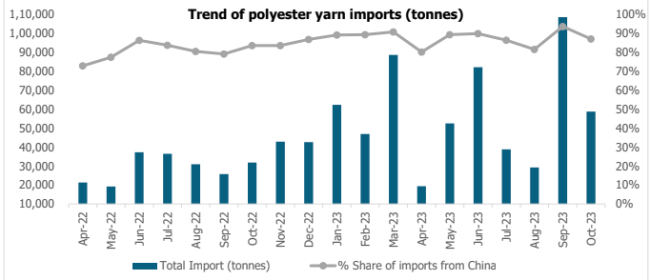

Although BIS was initially scheduled to be implemented in April 2023, the GoI postponed it twice (first in April 2023 and later in July 2023), with the implementation eventually taking effect from October 05, 2023. Notably, imports of polyester yarn witnessed a significant surge in September 2023, before the implementation of the QCO. This surge can be attributed to the pre-buying of polyester yarn by the downstream industry. A similar trend was also observed during March 2023 and June 2023 before the then-expected implementation of QCO.

Post BIS implementation, import of polyester yarn witnessed significant decline of nearly 60% in the month of November 2023 as compared to November 2022. Consequently, CareEdge Ratings expects a further reduction in polyester yarn imports in coming months which is expected to allow industry players to take some price increases. However, there is an exemption for compliance of BIS requirement against the advance license mechanism which may lead to some import of polyester yarn into India. With a potential improvement in average sales realisation along with stable raw material prices, the spread of polyester yarn is likely to improve (see Table 3).

Caption for the image: Table 3: Trend of polyester yarn imports (in tonnes)

Source: CMIE; Compiled by CareEdge Ratings

Profitability likely to improve from Q3FY24 backed by import reduction

With the expected improvement in polyester yarn spread, PBILDT margin is expected to gradually improve from Q3FY24 onwards. The improvement in operating profitability during Q3FY24 is expected to be constrained to some extent due to the pre-buying of polyester yarn before the implementation of BIS and a gradual increase in prices by industry players.

However, a more meaningful improvement is expected from Q4FY24 onwards. Additionally, with the resurgence in domestic demand in China as well as in key developed economies i.e. the USA and Europe, in the near to medium term, the demand-supply gap is expected to narrow and in turn, revive export demand for Indian players.

Key monitorables

- Possibility of import of polyester fabric instead of polyester yarn, as polyester fabric is not covered under BIS requirement as of now.

- The potential granting of BIS certificates to foreign yarn manufacturers is to be seen.

- Any major volatility in raw material prices which are crude derivatives.

CareEdge Ratings View

Table 4: Improvement in PBILDT margin (%)

“With an expectation of curtailment in import of polyester yarn and consequent increase in average sales realisation, PBILDT margin of Indian polyester yarn players is expected to improve from Q3FY24 and materially from Q4FY24 onwards. Overall, the Indian polyester yarn industry is expected to witness around 100 bps improvement in PBILDT margin during FY24 over FY23 and around 200 bps improvement during FY25 over FY24 (see Table 4), thereby reaching pre-COVID level. However, any major inventory mark down due to sharp decline in crude oil prices may result in lower than estimated improvement in PBILDT margin,†said Krunal Modi, Associate Director at CareEdge Ratings.

“With an expectation of curtailment in import of polyester yarn and consequent increase in average sales realisation, PBILDT margin of Indian polyester yarn players is expected to improve from Q3FY24 and materially from Q4FY24 onwards. Overall, the Indian polyester yarn industry is expected to witness around 100 bps improvement in PBILDT margin during FY24 over FY23 and around 200 bps improvement during FY25 over FY24 (see Table 4), thereby reaching pre-COVID level. However, any major inventory mark down due to sharp decline in crude oil prices may result in lower than estimated improvement in PBILDT margin,†said Krunal Modi, Associate Director at CareEdge Ratings.