Stable cotton prices due to better availability of cotton during cotton season 2024 and improved cotton yarn spreads this fiscal will support improvement in margins.

After a year of turmoil last fiscal, the cotton yarn spinning industry is expected to witness a breather this fiscal. Operating margins of cotton yarn spinners are set to improve by 150-200 bps this fiscal after hitting decadal lows of 8.5-9 per cent last fiscal.

In fiscal 2024, profitability was affected by lower cotton yarn spreads1 and inventory losses. This fiscal, however, holds better promise. Stable cotton prices due to better availability of cotton during cotton season 2024 and improved cotton yarn spreads this fiscal will support improvement in margins.

Revenue, too, will spin up 4-6 per cent this fiscal, driven by moderate growth in downstream demand amid stable yarn prices, after a 5-7 per cent decline last fiscal due to a sharp reduction in yarn prices.

Credit profiles, which were impacted by lower cash accrual last fiscal, will also improve with better operating performance and moderate capex on deleveraged balance sheets.

An analysis of 95 cotton yarn spinners, which account for 35-40 per cent of the industry revenue, indicates as much.

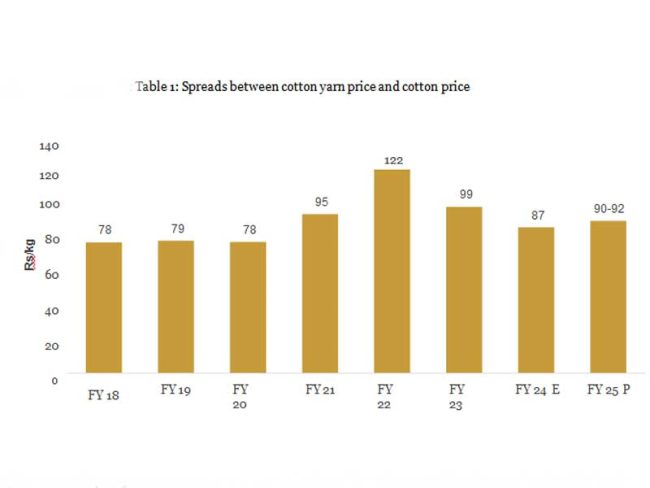

Says Gautam Shahi, Director, CRISIL Ratings, “Better availability of domestic cotton and continued downstream demand growth will drive recovery in cotton yarn spreads to Rs 90-92 per kg this fiscal from Rs 87 per kg last fiscal (Table 1 in annexure). The improvement was already visible in the second half of fiscal 2024 as higher cotton arrivals resulted in normalisation of cotton prices, thereby improving the margins of spinners. With cotton prices expected to stay benign and likely to remain below international prices, the operating margin is expected to recover 150-200 bps to 10.5-11 per cent this fiscal.â€

On the revenue front, while yarn prices are expected to remain flat, domestic sales volume, which forms 70-75 per cent of the industry pie, is set to grow 4-6 per cent this fiscal, backed by orders from key end-user segments – readymade garments and home textiles. However, exports, which staged an exceptional recovery last fiscal with 80-85 per cent growth, are likely to grow only 3-4 per cent this fiscal, given sluggish global economic growth. With recovery in demand and operating performance, capacity utilisation level for the industry has reached 80-85 per cent and is expected to improve further this fiscal.

Says c, Associate Director, CRISIL Ratings, “However, capex for cotton yarn spinners will remain moderate over the near term as they recover from lows of last fiscal, thus obviating the need for significant debt additions on already deleveraged balance sheets. As a result, interest coverage2 ratio is expected to improve to 5-5.5 times this fiscal from ~4 times in fiscal 2024. Gearing3, too, is expected to improve moderately to 0.55 time from 0.64 time.â€

However, any further slowdown in demand from the downstream segments (such as readymade garments), and any adverse movement in domestic cotton prices vis-Ã -vis international prices in the near term will bear watching.