President Trump’s stance from his previous term on reducing dependency on China is likely to strengthen India’s position in the US market in the medium term, informs Krunal Modi and Akshay Morbiya.

The Indian textile industry, being moderately reliant on exports, saw a 10 per cent decline in exports in CY23 due to impact on consumer demand arising from high inflation and rising interest rates, but it recovered by 6 per cent in 10MCY24. Gains in CY24 include shift in orders from Bangladesh and government measures to protect the Indian polyester yarn industry. Missed opportunities involved delays in the India-UK FTA and weak response to PLI 1.0. The Indian textile industry is expected to grow by 8-9 per cent in CY25, especially if cotton and polyester yarn (being crude oil derivative) prices remain relatively stable and forex rate is favourable, which could improve the operating profitability of textile players by 40-80 bps.

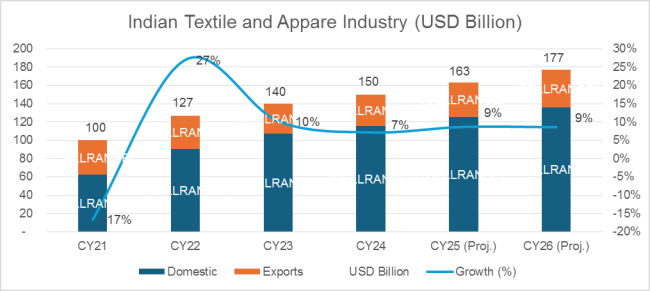

With export accounting for ~25 per cent of the Indian textile industry, global demand plays a crucial role in influencing the prospects of the industry. The home textile, readymade garment (RMG), and cotton yarn segments of the Indian textile industry derive 70-75 per cent, and 25-30 per cent each of their revenue, respectively, from exports. While domestic demand remained steady over the past two years, export demand faced challenges due to high inflation and rising interest rates in key export markets, adversely impacting demand. India’s textile and apparel exports stood at $ 32.8 billion in CY23 (refers to the period from January 01 to December 31), a decline of 10 per cent over CY22. After witnessing a decline, exports recovered in 10MCY24 and grew by 6 per cent on a y-o-y basis to $ 29.26 billion.

Indian textile and apparel industry (in $billion)

Source: Ministry of Textiles and CareEdge Ratings

Indian textile industry’s performance in CY24

Cotton yarn exports declined by 5 per cent in 11MCY24 over a relatively high base of 11MCY23, as 33 per cent growth in Bangladesh exports was offset by a 61 per cent de-growth in exports to China on a year-on-year basis. Cotton yarn exports depend on the parity of raw cotton prices in domestic and international markets. Domestic cotton prices largely remained higher than international prices since April 2024, which adversely impacted export of cotton yarn from India. Additionally, China’s textile industry also faced a slowdown in domestic consumption, which coupled with muted global demand for textile products, and the China+1 strategy being adopted by global suppliers and brand owners, impacted India’s cotton yarn exports to China. Despite the decline in exports, India’s cotton yarn production and sales volumes remain largely stable as the RMG, and home-textile sector have seen a notable recovery. RMG exports grew by 7 per cent in 11MCY24 on a Y-o-Y basis and stood at $ 13.2 billion, mainly supported by growth in exports to major consuming nations like the US and UK which together constituted nearly 43-45 per cent of total Indian RMG exports.

Gains and missed opportunities in 2024

The gains from 2024 are as follows;

Benefit from the Bangladesh crisis: Bangladesh occupied the 2nd position in global RMG segment with around ~8-9 per cent market share, while India stood a distant 7th with a market share of ~3 per cent in 2023. However, the socio-political disturbances erupting in Bangladesh during 2024 have shifted some RMG orders to India. India’s RMG exports have consistently outpaced that of Bangladesh’s since the onset of the above-mentioned crisis. India’s RMG exports grew by ~13 per cent in Q3CY25 while that of Bangladesh declined by 1 per cent during the period on a Y-o-Y basis. India continued to grow at a higher pace compared to Bangladesh even in October 2024.

Safeguards provided to domestic polyester yarn industry: To safeguard the domestic polyester yarn industry against import of cheaper and inferior quality products, the Government of India (GoI) implemented a quality control order (QCO) from October 2023 on polyester yarn, which has curtailed polyester yarn imports into India by 59 per cent (67 per cent from China) during Oct’23 to Sep’24 on a year-on-year basis. The GoI further imposed a minimum import price (MIP) on synthetic knitted fabrics in March 2024 to curtail cheaper imports of inferior quality polyester fabric, which was extended till December 31, 2024.

The missed opportunities are as follows;

Delay in the signing of FTA with UK: The India-UK Free Trade Agreement (FTA) negotiations started in January 2022 and originally set for completion by Diwali 2022 are progressing far behind schedule. The delay is due to political changes in the UK, elections in both countries and some key issues that remain unresolved after 14 rounds of negotiation to date.

Weak response to PLI 1.0: Under PLI 1.0, nearly 73 applicants were selected with a proposed investment of Rs 283.87 billion against which eligible investment made under the scheme was just Rs 33.62 billion as of March 31, 2024. Considering the weak response for PLI 1.0, PLI 2.0 is awaited after more than a year. Despite industry demand to include cotton garments and lower the criteria for minimum investment and turnover, no notable changes were made during the second application round of PLI 1.0.

Expectations for 2025

There has been a growth in RMG and home textile exports in the past few months following the stabilisation of inflation and interest rate cut prompting global brands and retailers to replenish their lean inventories. Additionally, political instability and increasing labour costs in competing nations, along with the increasing adoption of the China+1 strategy, shall support Indian textile exports in the near to medium term.

India’s textile exports are expected to grow by 6 per cent in 2024 to $ 34.75 billion and further grow by ~8-9 per cent and remain over $ 37-38 billion in 2025. RMG exports are expected to grow by 7 per cent in 2024 to $ 15.5 billion and further to grow by 12-13 per cent to reach $ 17-18 billion by 2025. Domestic demand for RMG is expected to grow by 9-10 per cent in 2025.

The home textile segment is expected to grow by 8-10 per cent in 2025, supported by stable cotton prices and increased demand from key importing countries, primarily the US.

Domestic demand for cotton yarn will outpace exports in the near to medium term, driven by recovery in downstream segments. Despite the decline in cotton yarn exports, increased demand from RMG and home textiles should support the overall demand for cotton yarn. Cotton yarn exports are expected to remain lower by 5 per cent in 2024 and are expected to grow by 2-3% in 2025. Overall, cotton yarn volumes are expected to grow by 5-6 per cent in 2025, primarily due to strong domestic demand.

If the Bangladesh crisis persists, India is expected to gain around 6-8 per cent of Bangladesh’s monthly export orders in the near term, translating into a monthly incremental export opportunity of around $200-250 million. Although cost is an important factor in the selection of suppliers for major apparel brands, the reliability of supply is also critical. Considering the ongoing social unrest in Bangladesh, apparel brands and retailers are looking for reliable alternative suppliers, which is evident from the recent surge in India’s RMG exports. Industry players have seen strong growth in inquiries and order inflows during the last few months. Companies with adequate capacities, especially in knitted garments, are expected to benefit the most. While in the short term, India can absorb the immediate demand, the medium to long-term benefits would be contingent upon building additional capacities, strengthening the supply chain, and becoming more cost-efficient.Operating profitability to improve marginally: Higher sales volume, expectation of stable cotton and crude oil prices along with a favourable forex rate, is likely to benefit the Indian textile industry’s operating profitability by 40-80 bps in FY25 and FY26. Improvement in operating profitability and controlled debt level is likely to result in an improvement in interest coverage ratio to 3.5x and 3.8x in FY25 and FY26 respectively.

Indian textile and apparel industry (in $billion)

Source: Ace equity; financial results of listed textile companies.

Likely FTA with the UK: The government of India may sign the FTA with the UK in 2025 which shall enhance the competitiveness of Indian exporters.

Launch of PLI 2.0: While the existing PLI scheme for textile sector, introduced in 2021, is limited to the production of man-made fibre (MMF) fabrics and apparel and technical textiles, PLI 2.0 is likely to cover garments, made-ups and accessories of all input material, including cotton.

Key monitorable

A proposed hike in GST for apparel may impact domestic demand for RMG. Moreover, any major change in the tariff structure by the incoming US Government may temporarily impact demand for Indian textile products. However, President Trump’s stance from his previous term on reducing dependency on China is likely to strengthen India’s position in the US market in the medium term. Lastly, the parity of domestic cotton prices with international cotton prices would also be crucial.

About the authors:

Krunal Pankajkumar Modi is a seasoned professional with over 16 years of experience at CARE Ratings . As the Director and Rating Head of the Large Corporate Team, he brings a wealth of expertise in financial analysis and corporate ratings.

Akshay Dilipbhai Morbiya brings around 8 years of experience at CARE Ratings, where he is the Assistant Director and Group Head of the Large Corporate Team. He specialises in financial analysis, corporate ratings, and industry research, and holds an MBA in Finance.