DTY Jet insert APe043 redefines low denier yarn processing

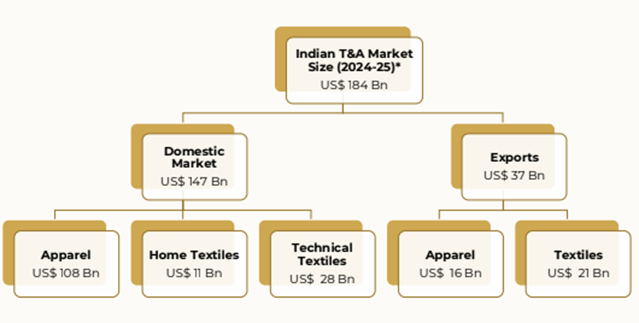

Within the domestic market, apparel leads with a substantial share of $108 billion, followed by technical textiles at $28 billion, and home textiles at $11 billion.

As per Wazir Advisors’ Annual Textile & Apparel Industry Report 2025, the Indian Textile and Apparel (T&A) market is projected to reach an impressive size of $184 billion by the financial year 2024-25. This growth is driven by two major segments: the domestic market and exports. The domestic market is expected to dominate with a valuation of $147 billion, showcasing the robust demand within India. Within this segment, apparel leads with a substantial share of $108 billion, followed by technical textiles at $28 billion, and home textiles at $11 billion.

On the export front, the Indian T&A industry is estimated to generate $37 billion. Apparel exports account for $16 billion, reflecting India’s position as a key global supplier of garments. Meanwhile, textiles contribute $21 billion, underlining the country’s stronghold in raw materials and finished fabrics.

The technical textiles sector, both in domestic and export markets, stands out as a significant contributor to the industry’s overall growth. With applications spanning multiple industries such as healthcare, infrastructure, and automotive, this sector is rapidly gaining momentum.

T&A market size (2024-25)*

Source: Wazir Advisors

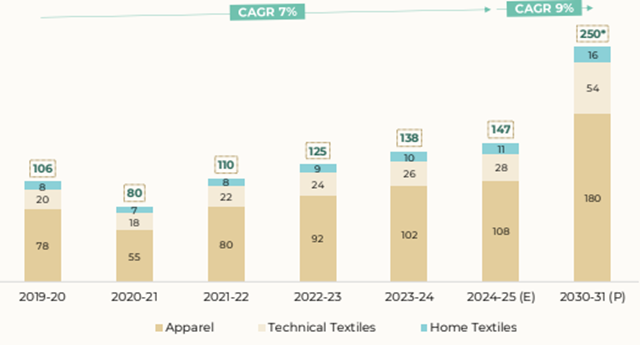

The apparel sector remains the backbone of the industry, growing from $78 billion in 2019-20 to an estimated $108 billion in 2024-25 and further surging to $180 billion by 2030-31. This underscores the increasing domestic and global demand for Indian apparel.

Technical textiles, a key driver of innovation, are also gaining prominence, with their market size expected to expand from $20 billion in 2019-20 to $28 billion in 2024-25 and $54 billion by 2030-31. The growth in this segment reflects its versatility and application in diverse industries such as automotive, healthcare, and infrastructure.

The home textiles segment, although smaller, has shown consistent growth, increasing from $8 billion in 2019-20 to $11 billion in 2024-25 and is projected to reach $16 billion by 2030-31. This reflects growing consumer preferences for premium home furnishing products.

These figures highlight the sector’s resilience, adaptability, and potential for future expansion. By capitalising on technological advancements, sustainability, and policy support, the Indian T&A industry is poised for remarkable growth in the coming years.

Sector wise projection

Source: Wazir Advisors

Major developments in 2024

The year 2024 witnessed notable developments that shaped the Indian textile and apparel industry. After a prolonged period of sluggish growth, textile and apparel exports finally showed signs of recovery in FY2024-25. Although this rebound brought much-needed optimism, the overall growth over the last five years remained modest, registering a compound annual growth rate (CAGR) of just 2 per cent. Exporters and industry stakeholders acknowledged this recovery as a step forward but recognised the need for sustained efforts to accelerate growth.

Another significant highlight of the year was the heated debate surrounding Quality Compliance Orders (QCOs). These regulations, aimed at improving product standards in the textile value chain, sparked mixed reactions. Stakeholders across the supply chain were divided, with some strongly supporting the move to ensure higher quality, while others raised concerns about its potential impact on costs and timelines. The implementation of QCOs for both manmade fibres and cotton, however, was deferred by a year, providing stakeholders additional time to align with these requirements.

On the consumer front, the demand for sportswear and athleisure garments soared, driven by a growing emphasis on health and fitness and a preference for comfort-centric apparel. This category experienced rapid expansion, with organised brands, ranging from direct-to-consumer (D2C) startups to large multinational corporations, reporting revenue growth between 15-20 per cent. This surge underscored the evolving lifestyle preferences of consumers and the sector’s growing importance in the broader apparel market.

Furthermore, several Indian states introduced revised or new textile sector policies to foster growth in the industry. States such as Andhra Pradesh, Gujarat, and Tamil Nadu led the way with initiatives aimed at boosting investment, creating employment opportunities, and enhancing export performance. These policies were designed to attract domestic and foreign players, reinforcing the states’ positions as key hubs for textile manufacturing and innovation.

Collectively, these developments marked 2024 as a year of recovery, debate, and forward momentum for the Indian textile industry. As the sector gears up for the challenges and opportunities ahead, these milestones set the stage for further growth and transformation.

Key trends to watch in 2025

As 2025 approaches, several key trends are expected to shape the Indian textile and apparel industry. The persistent growth slowdown in recent years has intensified financial strain on smaller and inefficient companies, accelerating industry consolidation. This trend will likely favour businesses that emphasise vertical integration and capacity expansion, enabling them to scale operations and enhance competitiveness.

Additionally, the growth of mass market brands is anticipated to play a pivotal role. Retailers like Zudio, Vishal, V2, and V-Mart are capitalising on value-conscious consumers by offering affordable yet stylish apparel. Their focus on competitive pricing and expansion into smaller towns is reshaping the retail landscape, bridging the gap between premium and unbranded segments.

On the regulatory front, a potential increase in the GST rate on higher-priced garments has raised concerns across the industry. While this measure targets premium products, it could inadvertently affect demand for wedding wear, woolen garments, and handmade products, posing a risk to overall domestic demand.

Lastly, accelerating sustainability trends are becoming increasingly important as exporters adapt to growing pressures from Western markets. Larger domestic brands and their suppliers are following suit, prioritising eco-friendly production, resource efficiency, and circularity. These practices not only address evolving consumer demands but also align with global expectations, setting the stage for a more sustainable and competitive industry. Together, these trends underline a transformative year ahead for the Indian textile sector.

News source: Wazir Advisors