With fast-changing markets, consumption behaviour, and demand fluctuations, denim will keep changing too, informs Urvashi Sharma.

Denim has risen above its humble beginnings as practical clothing for manual labourers to become a cornerstone of modern fashion. Amidst the ever-changing landscape, denim has stood the test of time. With its enduring appeal and versatility, denim has become a timeless staple in wardrobes across the globe irrespective of gender, age, and status in the economic pyramid.

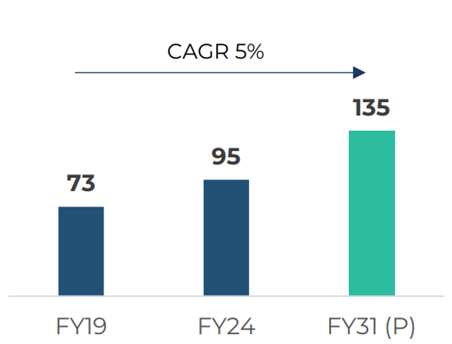

Global denim apparel market is growing at a moderate pace

The global denim apparel market, valued at $95 billion in 2024, has witnessed a 5 per cent CAGR over the past 5 years and is projected to reach $135 billion by 2031. This growth is driven by factors like increased retail channels, competitive pricing, urbanisation, a growing working-class population, and the acceptance of casual wear in office settings. The rising popularity of coloured denim and the continuous introduction of new styles further contribute to the expanding demand for denim.

Figure 1: Global denim apparel market (US$ bn)

Data Source: Wazir Advisors

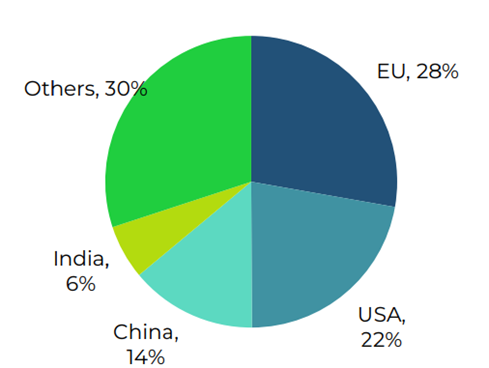

Figure 2: Key global denim apparel markets

Data Source: Wazir Advisors

While the market is projected to grow, there has been a recent downturn in major market demand

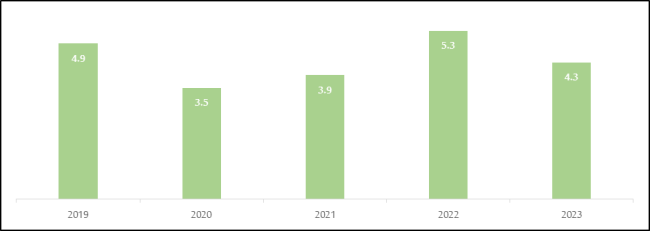

The EU and US remain the dominant markets, together making up half of global demand. The EU, holding approximately 28 per cent of total market demand, had denim apparel imports valued at $4.9 billion in 2019. This positive trend continued until 2022, but due to the recent geopolitical scenario, imports declined to $4.3 billion in 2023, reflecting a CAGR of -3 per cent.

Figure 3: EU Jeans Imports (US$ bn)

Data Source: Eurostat

The US is closely trailing with a market share of 22 per cent. Its denim apparel imports, valued at $3.6 billion in 2019, followed a similar trend to that of the EU, showing an upward trajectory until 2022. However, imports declined to $3.2 billion in 2023, reflecting a CAGR of -3 per cent. The fall in denim imports in two of the major markets for apparel and textiles, can be attributed to the sluggish demand in the markets due to economic slowdown triggered by the Russia-Ukraine war-induced high inflation that forced the consumers to prioritise their basic needs.

Figure 4: US denim apparel imports (US$ bn)

Data Source: OTEXA

Asian countries have risen as significant suppliers to fulfil the global garment demand

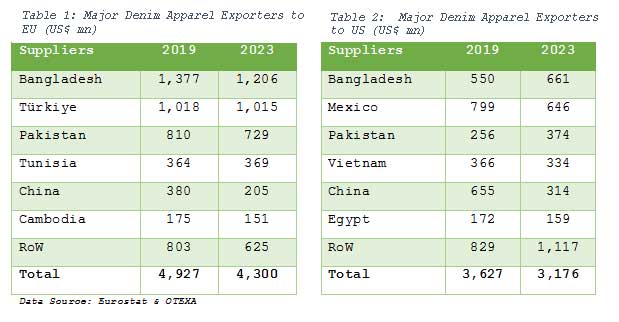

Key exporting nations such as Bangladesh, Türkiye, and Pakistan stand as prominent suppliers to the EU market. Among them, Bangladesh accounts for the largest share at 28 per cent, followed closely by Türkiye at 24 per cent, and Pakistan at 17 per cent. Free Trade Agreements (FTAs) play pivotal role for the EU market, particularly for Bangladesh, Pakistan and Türkiye granting them significant advantages and enabling them to become leading suppliers in the region. In the US market, a similar trend is evident, where Asian countries comprise over half of the imports. Bangladesh leads with the highest export share at 21 per cent, followed by Mexico at 20 per cent, Pakistan at 12 per cent, Vietnam at 11 per cent, China at 10 per cent and Egypt with a 5 per cent share. Türkiye’s proximity to the EU and Mexico’s proximity to the US has positioned them as the key suppliers.

As China experiences a decline in exports, other nations are seizing the opportunity. However, India is still in the process of fully capitalising on this shift. India’s exports to the EU market are relatively modest, registering a CAGR of -9 per cent. Similarly, in the US market, India demonstrates negative growth and holds a small market share.

Global trends shaping the industry

The denim industry is in a state of continuous evolution, driven by growing emphasis on various factors such as environmental concerns, geo-political issues and consumer preferences among others. Below are the key trends influencing the industry:

Sustainability has emerged as foundational trend across the value chain: In light of denim’s substantial environmental footprint, brands are prioritising eco-friendly practices and actively seeking out sustainable suppliers for collaborative efforts towards a more environmentally conscious industry across the denim value chain.

Brands are diversifying out of China: China’s combined denim apparel exports to the US and EU dropped from $1 billion in 2019 to $0.5 billion in 2023 at a -16 per cent CAGR, attributed to multiple factors like inflations, high labour cost, distrust b/w China and the West. Levi’s has significantly reduced the number of its Chinese suppliers by 72 per cent from 2019 to 2023. In line with its post-COVID sourcing strategy, Levi’s sourced from 32 countries worldwide in 2023 and does not obtain more than 30 per cent of its products from any single country[1]. Similarly, reflecting a broader trend among denim brands to reduce reliance on China, Guess decreased its dependence on Chinese suppliers from 43 per cent in 2019 to 31 per cent in 2023.

Another trend is the preference for vertically integrated suppliers by major brands. Major denim brands are also consolidating sourcing activities. The market has also witnessed a diversification in product offerings and consumer preferences, with a surge in demand for stretch denim for comfortable fits like leggings and joggers. Additionally, there’s a growing consumer demand for color variations beyond traditional Indigo.

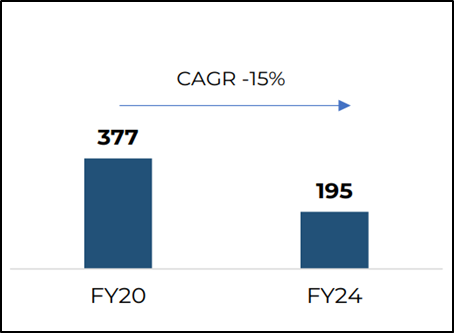

India’s exports of denim apparel are falling

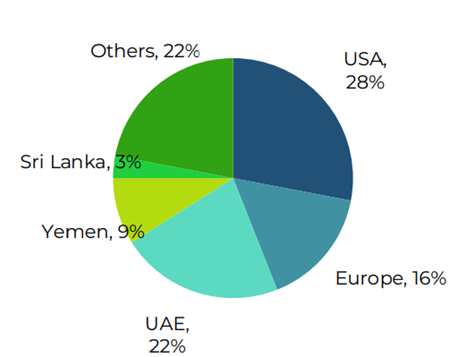

Currently, India has small share of 1 per cent in global denim apparel exports largely because denim apparel is domestic focused and there are only few large exporters. India’s denim apparel exports in FY24 were $195 mn. which has declined as compared to recent past largely due to global market challenges. Key markets for India are USA with a share of 28 per cent, followed by UAE (22 per cent) and EU (16 per cent).

Figure 5: India’s Denim Apparel Exports (US$ mn)

Figure 6: Key markets of India for denim apparel

Source: Wazir Analysis, Volza

The European Union (EU) and the United States (USA) are the largest importers of denim apparel, with a combined market value of $9.5 bn. Historically, China has been the leading supplier to these markets; however, due to geopolitical and other business factors, buyers are looking to diversify their sourcing to other countries. To capitalise on this trend and compete with other major exporters, India must focus on enhancing its denim apparel exports.

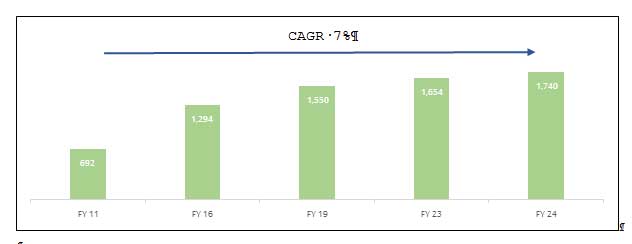

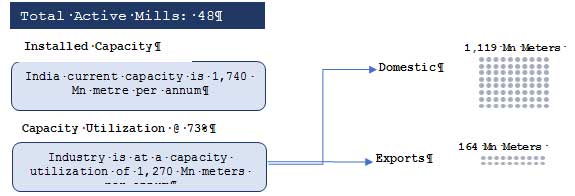

Manufacturing capacity has expanded over the years

India’s installed denim capacities have seen significant growth over the years. As of FY24, India boasts a substantial denim fabric manufacturing capacity of 1,740 million metres per annum (MMPA). Average CAGR of capacity growth since FY 11 is around 7 per cent. In last 5 years capacity has grown by 2.3 per cent CAGR. This growth trajectory includes the addition of around 90 MMPA in last year, demonstrating ongoing investments in expanding production capabilities. Currently there are 48 active mills operating at an average capacity utilization of 73 per cent.

Figure 7: Installed Denim Fabric Capacity (MMPA)

Data Source: DMA

Denim Industry is largely domestic focused as 88% of total fabric produced is used for domestic purpose. Historically, the industry has witnessed substantial growth of 7% since FY 11 in its domestic market consumption.

Figure 8: India’s Denim Fabric Domestic Consumption (Values in Mn. Meters)

Data Source: DGCI&S

This growing production in denim, provides India an opportunity to amplify its share in exports by strategically aligning with the global demand.

Indian denim industry has opportunities for accelerated growth

The Indian denim industry is on the brink of significant growth, offering opportunities for both existing players and new entrants. India’s denim apparel exports currently amount to US$ 195 Mn., there’s immense potential to increase that value. By optimizing underutilized capacity and converting fabrics into garments, India could potentially increase apparel exports by 7-fold. The “China +1†strategy also positions India as a viable alternative in the global supply chain. Following opportunities can be leveraged to boost garment exports:

Integrated and sustainable manufacturing facilities: Global brands are seeking integrated facilities for direct garment sourcing, streamlining their supply chain and ensuring consistent quality. India should invest in integrated garmenting units covering all production stages, from fabric creation to finished garments. This will attract more international brands and enhance capacity utilization and operational efficiency.

Free Trade Agreements: India has the potential to boost denim apparel exports to new FTA partner countries like Australia and UAE.

Supportive government policies: India has several supportive government policies which collectively create an enabling environment for the Indian denim industry to thrive at both domestic and international fronts.

Large domestic market: With a population exceeding 1.4 billion and dynamic fashion trends, India’s vast consumer base, coupled with a growing middle class, presents significant potential for the domestic denim industry.

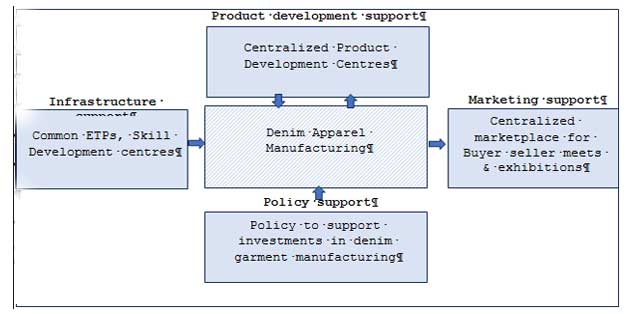

Figure 9: Creating Ecosystem for Denim Garment Manufacturing

To tap the outlined opportunities India can focus on the following strategies:

- Collaborations and partnerships: Collaboration for advanced technologies, integrated suppliers, and strategic collaborations for sustainable production.

- Product development and innovation: Embracing cutting-edge fabric technologies and customization options for global growth and competitiveness, solidifying its position on the global stage.

- Incorporating technology and automation: Embracing advanced technologies, such as 3D modelling, automated manufacturing processes, etc. to enhance efficiency, quality and market competitiveness.

- Compliance with International Standards: Compliance with international standards is crucial for global brands when selecting manufacturing partners. Factories meeting stringent norms in labour practices, safety, and environmental regulations are preferred. India should upgrade its garment factories to these standards, enhancing competitiveness and appeal to international brands, ensuring sustained business and growth.

In conclusion, denim is here to stay, and it will continue to evolve and expand. With fast-changing markets, consumption behaviour, and demand fluctuations, denim will keep changing too. By adopting strategic approaches, denim manufacturers must focus on garmenting and vertical integration to position themselves at the forefront of the global denim industry. They should leverage their strengths in innovation, sustainability, and cost competitiveness to become an integrated supplier, ensuring they stay ahead in this dynamic market.

About the author:

Le Lorem Ipsum est simplement du faux texte employé dans la composition et la mise en page avant impression. Le Lorem Ipsum est le faux texte standard de l’imprimerie depuis les années 1500, quand un imprimeur anonyme assembla ensemble des morceaux de texte pour réaliser un livre spécimen de polices de texte. Il n’a pas fait que survivre cinq siècles, mais s’est aussi adapté à la bureautique informatique, sans que son contenu n’en soit modifié.