Future on the Hanger

Today, the Indian garment industry hangs like a garment on a hanger-balanced between uncertainty and possibility. Divya Shetty explores how by identifying and seizing the right opportunities, India can not only stay ahead in the global race but also redefine its role as a leader in the world of apparel.

India’s garment industry is currently navigating a turbulent environment with notable resilience. Export performance is showing signs of steady recovery, supported by a 7 per cent increase in textile and apparel shipments between April and October of FY 2024–25. This growth is largely fuelled by strong contributions from ready-made garments (RMG) and man-made fabrics. India continues to be amongst the top five textile exporter and commanding around 4 per cent of global market share (see Table 1).

However, the industry is grappling with a range of complex challenges, including global trade uncertainty reflected in fluctuating shipping costs, inconsistent import duties, and evolving tariff structures.

Suketu Shah, CEO, Vishal Fabrics, says, “While US tariffs on competitors like Bangladesh and Vietnam may benefit India, they also introduce volatility in sourcing and pricing. Meanwhile, domestic policy changes such as cotton MSP hikes are raising raw material costs, compelling manufacturers to lobby for import duty relief to stay competitive. On the global front, the India–UK FTA promises duty-free access for Indian apparel and textiles, potentially boosting exports to the UK by 30–45 per cent but the gains depend on smooth implementation and regulatory hygiene .â€

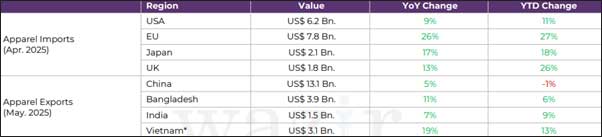

Table 1: Trade Statistics April-May 2025

This volatility has shifted manufacturing pressures onto cost structures and working capital.  According to Naveen Sainani, Founder and Chairman, Fritz Gaitri Clothing Co, “The market is largely MSME-based and primarily dependent on the domestic sector, which focuses heavily on high-street retail and local brands. However, with the rapid expansion of organised retail — especially brands like Zudio and others across Tier 1, 2, and 3 cities — competition has intensified. This has resulted in reduced footfall for high-street shops. On the other hand, many manufacturers are shifting to FOB (Free on Board) and private label business models, but these also operate on very thin margins. So overall, it’s a tough time for Indian garment manufacturers, both in the domestic and private label segments.â€

In domestic market, factors like labour shortages and inability to innovate and adapt are also one of the main obstacle in growth. As compared to domestic market, international market is still performing better. However, geopolitical factors have made exporters more cautious. Here are a few factors that have made the export situation more challenging.

Global trade uncertainty, manifested through fluctuating shipping costs, variable import duties, and shifting tariff regimes, has shifted manufacturing pressures onto cost structures and working capital.

Logistics in limbo

India’s garment export market is currently treading through a phase of uncertainty, with stakeholders adopting a wait-and-watch approach. While the industry has weathered many storms in the past, the current environment feels particularly unpredictable.

It is imperative that India negotiates trade terms that offer a level playing field. Additionally, exporters must closely monitor policy developments and diversify product offerings to stay competitive amidst any tariff realignment.

Bangladesh border blues: The India–Bangladesh trade relationship is in turmoil following a series of reciprocal restrictions. Bangladesh has suspended key imports like cotton yarn via land ports, prompting India to ban Bangladeshi RMG and jute through the same routes. Exports are now funnelled only via specific seaports, disrupting supply chains and escalating tensions. Rahul Mehta, Chief Mentor, CMAI, further highlights this uncertainty by stating, “At present, there isn’t any significant disruption. However, some major Indian brands and retailers that were previously sourcing from Bangladesh are now shifting part of their orders to Indian suppliers. This shift is primarily due to two reasons; With the latest restrictions, importing from Bangladesh has become approximately 4–5 per cent more expensive. The lead time has increased by 8–10 days, which affects delivery schedules. As a result, many buyers are choosing to divert some of their sourcing to domestic vendors.

India has restricted apparel imports from Bangladesh to only pass through southern ports, whereas earlier, shipments arrived via Kolkata, which was logistically cheaper. This new routing adds to transportation costs. Additionally, Bangladesh’s domestic manufacturing costs are steadily rising due to increasing minimum wages and other operational costs. Although it still remains cheaper than India, the gap is narrowing.

Bangladesh has also faced allegations of re-exporting Chinese fabrics to India at lower prices. Sainani quotes, “There has been strong opposition to the duty-free import of garments from Bangladesh, which are largely made using Chinese fabrics and accessories. Bangladesh, which does not produce its own yarn or fabric, imports these materials — mainly from China — and then re-exports them as finished garments. These finished products are entering India duty-free, putting Indian manufacturers at a disadvantage.â€

Tariff tremors from the US: India’s garment industry is facing a wave of turbulence in the wake of revised US tariff rates. Exporters are grappling with mounting uncertainty, prompting strategic reassessment across production, pricing, and market outreach. As strategies evolve, the sector braces itself for potential disruption and reorganizes to safeguard its hard-won export resilience.

Dr Mukesh Kansal, Chairman, CTA Apparels, views the situation with a mix of optimism and concern, as he remarks “The revised US tariff structures pose both opportunities and challenges. On one hand, any reduction in duties for Indian products can be a major booster for our exports to the United States, which remains our largest apparel market. On the other hand, if preferential tariffs are extended to competing nations without reciprocal benefits for India, we risk losing market share. It is imperative that India negotiates trade terms that offer a level playing field. Additionally, exporters must closely monitor policy developments and diversify product offerings to stay competitive amidst any tariff realignment.â€

In real terms, this affects our pricing strategy, inventory planning, and cash flow cycles. To adapt, the companies are exploring diversified markets, negotiating longer-term contracts with customers, and engaging with the government to fast-track tariff relief. Ultimately, the current environment demands both agile execution and close policymaker engagement.

Shah explains, “As the head of a textile firm, I see the US revising its tariff structure as both a challenge and a strategic pivot point. The current 26 per cent reciprocal tariff on Indian textile imports significantly raises our landed costs. That spells immediate pressure on margins, either we absorb some of the burden, or we pass it on, risking US order volumes. Yet, these higher tariffs also lean in our favour compared to rival exporters- while we face 26 per cent, competitors like Vietnam (46 per cent), Bangladesh (37 per cent), and China (34 per cent) are hit harder. Clients in the US are starting to shift orders from those destinations to India, and our textile stocks even saw an uptick immediately after the announcement. However, uncertainty remains high. The US has paused the implementation of higher duties, and a narrow “mini-deal†with India could be reached by the end of July that may reduce our trade friction to under 20 per cent.â€

Impact of India-UK FTA: The UK–India Free Trade Agreement (FTA) represents a significant milestone for India’s garment industry. With the removal of tariffs ranging from 12–16 per cent on apparel exports to the UK, nearly all Indian garments will gain duty-free access—on par with competitors like Bangladesh and Vietnam. This is expected to drive a 30–50 per cent surge in exports to the UK over the next five years. The agreement presents a major opportunity for India’s key textile hubs, which are heavily SME-driven and provide employment to millions. Reduced duties will enhance the price competitiveness of Indian products, allowing exporters to improve profit margins or offer more competitive pricing.

However, the agreement must clear Parliament in both countries, implementation could be delayed by up to a year. Exporters must also meet rules-of-origin and quality standards, and ensure compliance with UK regulations reopening trade channels.

“Longer term, the FTA supports India’s ambition to double its trade with the UK to US $100–120 billion by 2030. The garment industry stands to gain on employment, investment, and global integration, provided it modernises production, strengthens compliance infrastructure, and prepares itself for a ramp-up in volume and quality standards in a competitive UK market,†comments Shah.

Sainani also feels that the India-UK Free Trade Agreement will be a very positive move and is expected to benefit the Indian garment industry significantly, particularly in enhancing regional trade and competitiveness.

According to Kansal, “The European Union and the United Kingdom stand out as promising alternatives. These markets offer transparent trade regimes and are placing heightened emphasis on sustainability, ethical sourcing, and compliance. Their structured and predictable procurement models, coupled with a growing demand for high-value products, make them compelling destinations for both risk diversification and long-term growth.â€

Beyond the commercial upside, the FTA is expected to generate employment, foster domestic value addition, and promote the adoption of sustainable and ethically aligned manufacturing practices in line with international benchmarks

While the UK is not as large a market as the US or EU for Indian garments, it’s still a significant importer. Previously, countries like Bangladesh had a competitive edge in the UK market. Now, with the FTA, Indian exporters can compete more effectively. As for UK garments entering India, those are typically high-end products and unlikely to pose serious competition to domestic players.

Eyeing India-US FTA: While discussions of India-US FTA have intensified in 2025—with multiple rounds of talks completed and a roadmap outlined by both governments—a full-fledged FTA remains under negotiation. An interim trade deal was expected, but recent reports suggest delays due to disagreements on tariff structures, labour standards, and digital trade rules. Both sides remain engaged, aiming for a mutually beneficial agreement, though the timeline for a formal FTA remains uncertain. But the industry is truly looking forward for this FTA as it can drastically change the landscape of Indian garment industry.

Mehta explains, “If implemented, an India-US FTA would be a true game changer. Currently, the US accounts for 30–35 per cent of India’s total apparel exports. Duty-free or reduced-duty access, especially compared to competitors like Bangladesh, China, Vietnam, and Cambodia, would offer Indian exporters a huge advantage. Even MSMEs would benefit, as many exporters source their goods from them. Moreover, MSMEs that meet compliance standards could directly export to the US as well.â€

Kansal, on the other hand, points out that these on-going discussions are affecting the logistics of garment movement. He says, “The on-going ambiguity surrounding the India–US Free Trade Agreement is beginning to cast a shadow over India’s apparel export landscape. In the absence of a clear and consistent policy framework, global buyers are growing increasingly cautious. This hesitancy is translating into deferred commitments, shorter procurement cycles, and tighter lead times, making it harder for Indian exporters to remain price-competitive, especially against peers in nations with established trade agreements with the United States.â€

The domestic drag

Growth has slowed. While the sector is still expanding, the expected pace hasn’t materialised. Consumers are increasingly moving toward value-for-money products, and even premium brands are resorting to discounts and aggressive promotions to stay competitive. This trend has led to a dip in realisations and margins. Here are a few factors that are impacting the domestic market;

- Rising input costs: Fluctuating prices of raw materials like cotton and man-made fibres are squeezing profit margins.

- Labour shortages: Key garment hubs such as Tiruppur and Ludhiana are facing a lack of skilled workers due to migration and demand-supply gaps.

- Infrastructure bottlenecks: Inadequate logistics, transportation delays, and limited warehousing capacity increase production costs and lead times.

- Limited access to finance: Many SMEs, which dominate the industry, struggle with working capital and access to credit, despite supportive schemes.

- Policy and compliance challenges: Frequent changes in GST, quality control orders, and regulatory norms create uncertainty and increase compliance burden.

- Changing consumer preferences: The rise in demand for sustainable and fast fashion is forcing manufacturers to innovate quickly, often at higher costs.

- Digital and tech adaptation: Although many players are embracing automation and digitalisation, smaller units find it difficult to invest in new technology.

- Impact on competitiveness: These domestic hurdles limit the industry’s ability to compete globally and make the most of emerging export opportunities.

Future-proofing the industry

To boost garment exports in today’s global trade scenario, we need a clear, multi-pronged approach. “First, simplify incentives like RoDTEP and RoSCTL, ensure these schemes are transparent, easily accessible, and linked to quick real-world benefits for exporters rather than complex paperwork. Second, to accelerate Free Trade Agreements, both the UK‑India and approaching US negotiations must be turned into firm reorder advantages by eliminating tariffs at the earliest. Tariff-free access will directly translate into improved order flow and pricing power. Third, investing in cluster-based infrastructure improvements, upgraded common facility centres, logistics hubs, and cold chains near garment clusters will reduce lead times and shipping costs. That builds a factory-ready ecosystem. Fourth, support technology adoption among SMEs, offer rebates for automation, compliance tools, and digital platforms so smaller units can meet global standards in quality and delivery,†concludes Shah.

Measures such as strengthening trade diplomacy, leveraging Indian Missions for real-time market intelligence, addressing sudden non-tariff barriers, and facilitating dispute resolution for exporters can significantly streamline export processes. Combined with enhanced export incentives, effective FTAs, improved infrastructure, SME support, and proactive international engagement, these steps can position India’s garment industry for sustained global growth.

Sainani also suggests that the government needs to focus on developing micro-clusters rather than only large-scale projects. While initiatives like the PLI scheme for investments above Rs 1 billion are welcome, about 95 per cent of Indian garment manufacturers fall under the MSME category. A targeted approach with policies, subsidies, and compliance support for MSMEs will go a long way in enhancing their capabilities, especially in exports. Empowering the MSME sector is critical for the overall growth of the Indian garment industry.

Mehta expresses confidence in the future of the Indian garment industry, stating that, “The long-term future remains bright. India has a growing, young population, rising urbanisation, and a robust GDP growth trajectory. However, businesses will need to evolve. Models must shift, and companies must adapt to changing market dynamics. Those who fail to keep up may struggle, but the industry as a whole is poised for sustained growth.â€

The Indian garment industry stands at a promising juncture, with several opportunities ready to be tapped. With its vast workforce, strong manufacturing base, and growing global reputation for quality, India has the potential to become a global apparel hub. Rising demand for sustainable fashion, shifting sourcing preferences from global buyers, and ongoing trade negotiations like FTAs present a golden window. By investing in innovation, upskilling labour, adopting green technologies, and improving ease of doing business, the industry can unlock higher growth. Enhanced collaboration between government and industry stakeholders will further pave the way for a resilient ecosystem.

Today, the industry hangs like a garment on a hanger—balanced between uncertainty and possibility. By identifying and seizing the right opportunities, India can not only stay ahead in the global race but also redefine its role as a leader in the world of apparel.